+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

The research aims to identify the financial reality of the Iraqi General Reinsurance Company and identify its strengths to enhance it and weaknesses to address and improve it, as well as identifying appropriate financial criteria and indicators for evaluating the company's performance. The problem of the research was the company's inability to determine its financial reality and compare what was planned from the received premiums with what was achieved from them. The case study approach was relied on for the period (2010-2020) and the required data were collected using the planning and general budget and the annual reports of the company for the mentioned period. The researcher was reached a number of conclusions, the most important of which that the company suffers from weakness in the financial performance, as it witnessed a decline in the growth rate of reinsurance premiums, as well as a decrease in the revenues of reinsurance operations and the continued decline in the growth rate in the surplus, especially in the last years of the period under study, with a rise in the growth rate of compensation paid to the company due to weak review of reinsurance documents and the acceptance of high-risk documents.

The subject of performance appraisal has a great importance, as it is an approach to determine how institutions can achieve their goals, measure the efficiency of their performance and identify strengths and weaknesses to enhance the first and address the second. The financial performance evaluation based on many ratios and indicators through which the company's financial reality can be measures using the various financial statements. The insurance sector is one of the most important financial sectors and an essential component of the financial and economic sector of countries and with the increasing risks to which the individual is exposed, it becomes necessary to have insurance companies that play an important role in economic development and individuals resort to them to provide protection for them against risks that can be insured. In the insurance industry, so we will evaluate the financial performance of the reinsurance company in Iraq using financial indicators that are commensurate with the nature of the insurance business. The current research consists of three sections, the first section dealt with the research methodology, the second section presented the theoretical aspect related to the issue of reinsurance, while the third section showed the practical side of the research and presented the conclusions and recommendations that the research reached.

Research Problem

The research problem lies in the poor financial performance of the Iraqi reinsurance company and the lack of knowledge of its strengths and weaknesses and how to address them. Therefore, in light of the foregoing, the research problem can be stated by asking this question:

What is the reality of the state of financial performance in the Iraqi general reinsurance company?

How can the financial performance of the Iraqi general reinsurance company be evaluated?

Research Objectives

Identifying the reality of the state of the Iraqi general reinsurance company and identifying its strengths and weaknesses

Determine the appropriate financial criteria and indicators for evaluating the company's financial performance, which are commensurate with the nature of the insurance business

Analysis of the financial performance of the Iraqi General Reinsurance Company

Research Hypothesis

The Iraqi General Reinsurance Company suffers from poor financial performance and its inability to identify the strengths and weaknesses of the company and thus its inability to achieve its future goals.

Data Collection Methods

Reliance was made on Arabic and foreign sources and references such as books, articles and published research related to the subject of the research. The balance sheet, planning and annual report of the company for the period (2010-2020) were also relied on and presented in tabular form.

The Most Important Financial Indicators Related to the Insurance Activity

Insurance companies have characteristics that are unique to them from other companies due to the important role they play. Therefore, evaluating the financial performance of insurance companies requires special indicators in addition to traditional financial indicators. These indicators are:

Per Capita Productivity Development Rate

This indicator shows the productivity of one employee during the year and is extracted as follows [1]:

Wage Productivity Ratio

It is extracted from dividing the premiums achieved during the year by the salaries and wages for the same year, which are as follows [2]:

Insurance Premium Growth Rate

It is considered one of the important indicators that show the increase or decrease in the premiums achieved in the current year compared to the premiums achieved for the previous year:

The Rate of Growth in the Surplus or Deficit

The surplus or deficit was calculated from the following equation [3]:

Surplus or deficit = Insurance activity revenues-Insurance activity expenses

The percentage of growth in the surplus or deficit was calculated through the equation:

The Growth Rate of Compensation Paid

Compensations represent sums paid to the insured by insurance companies in the event that the insured risk materializes. The greater the amount of compensation, the lower the profitability of the companies and thus leads to poor financial performance and vice versa. It is one of the indicators that shows if there is an increase or decrease in the percentage of compensation paid during the year compared to the previous year and it is calculated through the following equation [4]:

Reserve Growth Rate

The reserve was considered a strong fortress for the shareholders and one of the factors affecting the financial performance, as it is formed to meet potential or certain obligations in the future and this ratio gives an indication of the reserves that were formed during the year and compared with the reserves of the previous year:

The Growth Rate of Investment Amounts

It is one of the indicators that express the volume of investments made by the company and is calculated through the following equation [1]:

Investment Revenue Growth Rate

Investments are necessary in improving the financial performance of insurance companies, as investment returns represent a major source of revenue for the company [4], which are the revenues that the company obtains from investing financial surpluses and are calculated according to the following equation [2]:

Gross Profit Growth Rate

This percentage reflects the financial position of the company, as its increase indicates an increase in the company’s activity and can be calculated as follows [5]:

The Theoretical Framework

Concept and Objectives of Performance Appraisal: Performance is a broad and essential concept whose components were renewed with the occurrence of any change or modernization in the components of the organization of all kinds. It shows the ability and ability of the organization to achieve its goals and measure the work accomplished within a specific period of time [6]. That it is a process of reviewing all the achievements achieved based on work standards and in accordance with the strategic goals and plans of the company. As for Abd Al-Rahim and Al-Wafi [7], it was mentioned that it described the current situation of the company and identified the fields that it used to reach the goals through studying revenues, assets, liabilities and sales. As for Al-Tarawneh [8], it was mentioned that it represents the company’s ability to achieve its financial goals, which is expressed through financial indicators such as liquidity, profitability and others, while Somaya [9] defined it as measuring results in the light of pre-defined criteria to determine what can be measured and then determine the extent to which goals are achieved and determine the relative importance between the results and the resources used.

The objectives of evaluating financial performance are as follows [10,11]:

Assisting decision makers in improving financial performance in a scientific and sound manner

Rationalizing the cost through the development of work and access to better methods of achievement at a lower cost

It aims to achieve cooperation between the units and divisions of the company that participate in the implementation

Working on developing the company and identifying its problems and solving them

Achieving compatibility with environmental variables, whether internal or external

Determine the stages of implementation and follow up the progress and development of work within the company

Factors Affecting Financial Performance

There are two types of factors that affect the financial performance, including internal and external, as follows:

Internal factors affecting the company's financial performance [12]

These are the factors that the organization can control and control, which are:

Control over the use of available resources

Cost control

Monitoring expenses during the various financial periods, indicating their importance to the company and trying to rationalize and correct them

External Factors Affecting the Company's Financial Performance

They are those factors that the company cannot control and control, as they result from changes in the external environment, as it is the external environment that generates them and these factors include [13]:

Technological and scientific changes that affect the quality of services provided by the company

Laws and instructions applied to the company by the state and market laws

In addition, there are other external factors, which are the economic factors that refer to the economic environment from the characteristics and elements of the economic system in which the company operates. Examples include unemployment rates, inflation, prevailing interest rates and some economic policies such as the monetary and financial policy of the state and economic variables such as the trend towards globalization and liberalization of the economy [8].

Internal and External Standards for Evaluating the Performance of Insurance Companies

There are internal and external standards for evaluating the performance of insurance companies, which are [14]:

External Standards: It is the one that the majority of dealers care about, as it bases its judgment on the insurance company and the most important of them is good service to customers, which is represented by speed and justice in the cost of insurance, compensation settlement and the general financial reputation of the company

Internal Standards: To set realistic and more specific criteria for measuring performance in the insurance company, we resort to evaluating the various administrative elements in the company and measuring the extent of their development and performance of their functions

The Objectives of Financial Analysis in Insurance Companies [2,6]

Evaluating the performance of economic units, increasing the current and future value of existing projects and increasing the expected value of new projects

Follow up the implementation of the set investment plan

Achieving appropriate returns on investment such as commercial profitability for existing and new projects, as they vary in economic systems such as central planning that focuses on external savings in terms of benefits and costs on the national economy when studying the financial evaluation of existing projects or new projects

The financial analysis provides quantitative and qualitative indicators that help the financial and economic planner in drawing financial, social and economic goals and preparing planning budgets and appropriate annual plans

The financial analysis compares the actual data and information with the planned data and information. It also identifies deviations, analyzes them and finds out their causes using technical methods

Definition of Reinsurance

The reinsurance is a contract concluded between the original believer (the assistant or direct believer) and between the reserve believer and is called the assignment of insurance, where the first is compensated by the second for the danger that the believer has pledged to, thus the direct believer or Al-Musnad can exempt himself through his conclusion. Insurance assistant [15]. It was also defined as a new and independent insurance contract based on the original insurance policy and it is at the same risk that was insured under the original insurance policy issued by the insurance company, as the reinsurer agrees to compensate the waived company for its potential loss in return for a premium of money paid by the waived company to the reinsurer [16]. Reinsurance also defined as a technical process by which the direct insurer insures part of the risks that he pledged to insure with another insurer for fear of his inability to compensate them and the direct insurance companies resort to reinsurance when insuring major projects or huge facilities that exceed their financial capabilities. They have a relationship with the reinsurance company. In the event of an accident, they demand the direct insurance company that signed the contract with them [17]. Figure 1 expresses the nature of reinsurance.

Characteristics of a Reinsurance Contract

The reinsurance contract includes many characteristics [18,19]:

It is a contract between the direct insurance company with which the insured carried out the insurance and the reinstatement company, where the insured is not a party to the contract but rather his relationship is with the direct insurer only who concluded the original insurance contract

The reinsurance contract is one of the causal contracts, its existence is linked to the existence of a previous insurance contract, as in the voluntary reinsurance and the conventional reinsurance

The reinsurance contract is a special contract related to the reinsurance of part or all of the risks on the money or one person insured or it is a general contract that includes coverage of all the risks that the outsourcing company has insured

The pillars of a reinsurance contract are the consent, the object and the cause and the subject is the reinsured part of the insured risk, so it is the responsibility of the entrusted company towards the insured in the insurance contracts

The reinsurance contract is one of the contracts of ultimate good faith, in which the direct insurer must provide the reinsurer with all information and data related to the risks that he reinsures, especially with regard to the nature of the risks and the previous experience of the direct insurer in such risks and a statement of the losses that occurred to the insurer. Al-Wardi [20] stated that there are other functions for reinsurance, which is that the reinsurer absorbs the pressure that insurance companies are exposed to as a result of large losses or unexpected medium and small losses and thus it provides protection for the following categories:

The insured has to face fluctuations in the cost of insurance protection represented by the insurance price. Through this method, the burden of losses is distributed over a number of years

Shareholders of insurance companies suffer from the significant decrease in the registered capital and this will provide them with a stable return that may become growing

For state finances, due to the ability of insurance companies to pay taxes

For workers in the insurance company from the risk of losing their work and the social benefits associated with it

Reinsurance Methods

There are two ways of reinsurance [21]:

Optional Reinsurance: It is the oldest method of reinsurance in which each reinsurance process is presented individually by the assigning company to the reinsurer, who has the option to accept or reject

Figure 1: Nature of Reinsurance

Source: Al-Wardi and Ali [20]

the reinsurance process and that the outsourcing company is the one who sends the data of the operation to be insured and the amount of reinsurance to the reinsurer or reinsurers who want to be reinsured with them, after deciding the amount of the original insurance that you keep and the direct insurer and the reinsurer are free to conclude or not conclude the contract and in this way the direct insurer can face unusual risks and obtain profits and It enables him to accept risks, no matter how big they are, as long as he can reinsure the parts that exceed his reserve capacity

Reinsurance Agreement: It is an advanced method in which the direct insurer is obligated to indicate to the reinsurer that part of the risk that is assumed within the limits of his retention from the general risks covered by the agreement and the reinsurer is obligated to accept this part and the responsibility of the reinsurer consists when concluding the original insurance contract between the direct insurer and the original insured

The Practical Side

The history of the Company: The Iraqi Reinsurance Company was established under Law No. 21 of 1960 and its articles of incorporation and by-laws were issued on 4/25/1960. The company started its operations on January 1, 1961 and with the issuance of the Public Companies Law, the company’s conditions were adapted in accordance with the provisions of Law No. (22) for the year 1997 according to the certificate of incorporation issued by the Registrar of Companies on February 28, 1998. This company is one of three governmental companies affiliated to the Ministry of Finance, as it is a self-financed economic unit that enjoys moral personality and administrative and financial independence. The company's total funds and reserves amount to (56,163) billion dinars, while the invested funds amounted to (51,326) billion dinars, which were distributed to various portfolios, including (real estate lending, owning and renting real estate, establishing companies inside and outside Iraq or contributing to their establishmen. (Source: The company's annual report for 2020).

Analysis of the Financial Performance of the Company using Financial Ratios Related to the Insurance Activity

Per Capita Productivity Growth Rate for the Company for the Period (2010-2020) (Table 1, Figure 2)

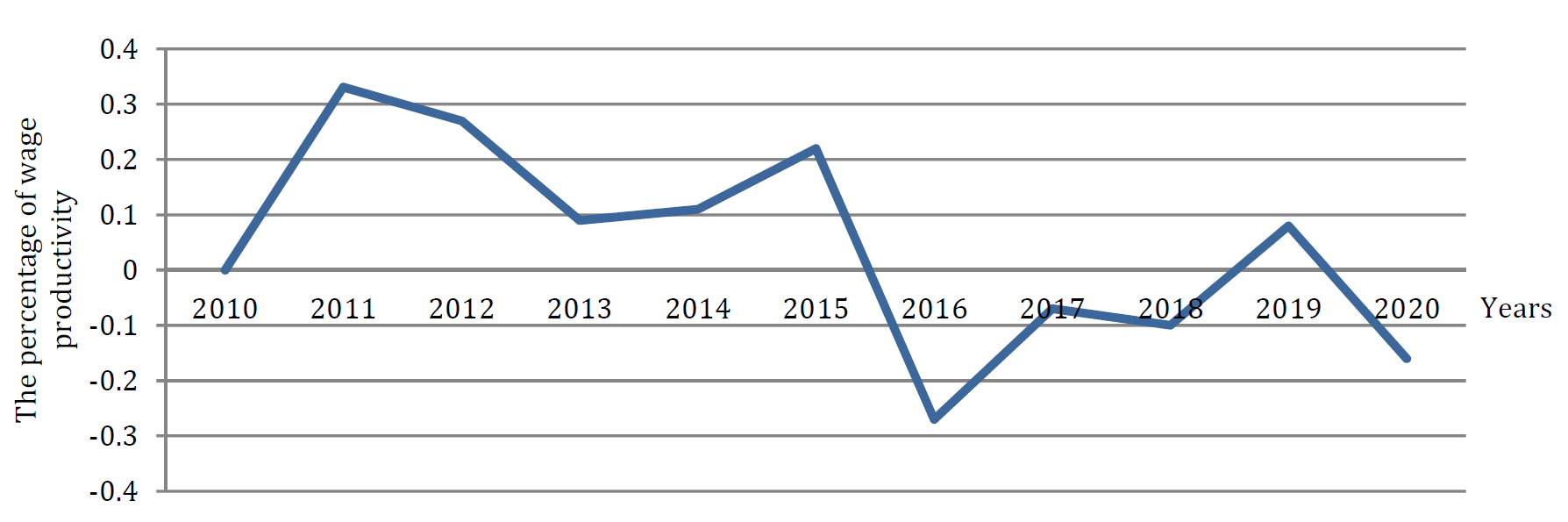

The percentage of wage productivity for the company for the period (2010-2020) (Table 2, Figure 3)

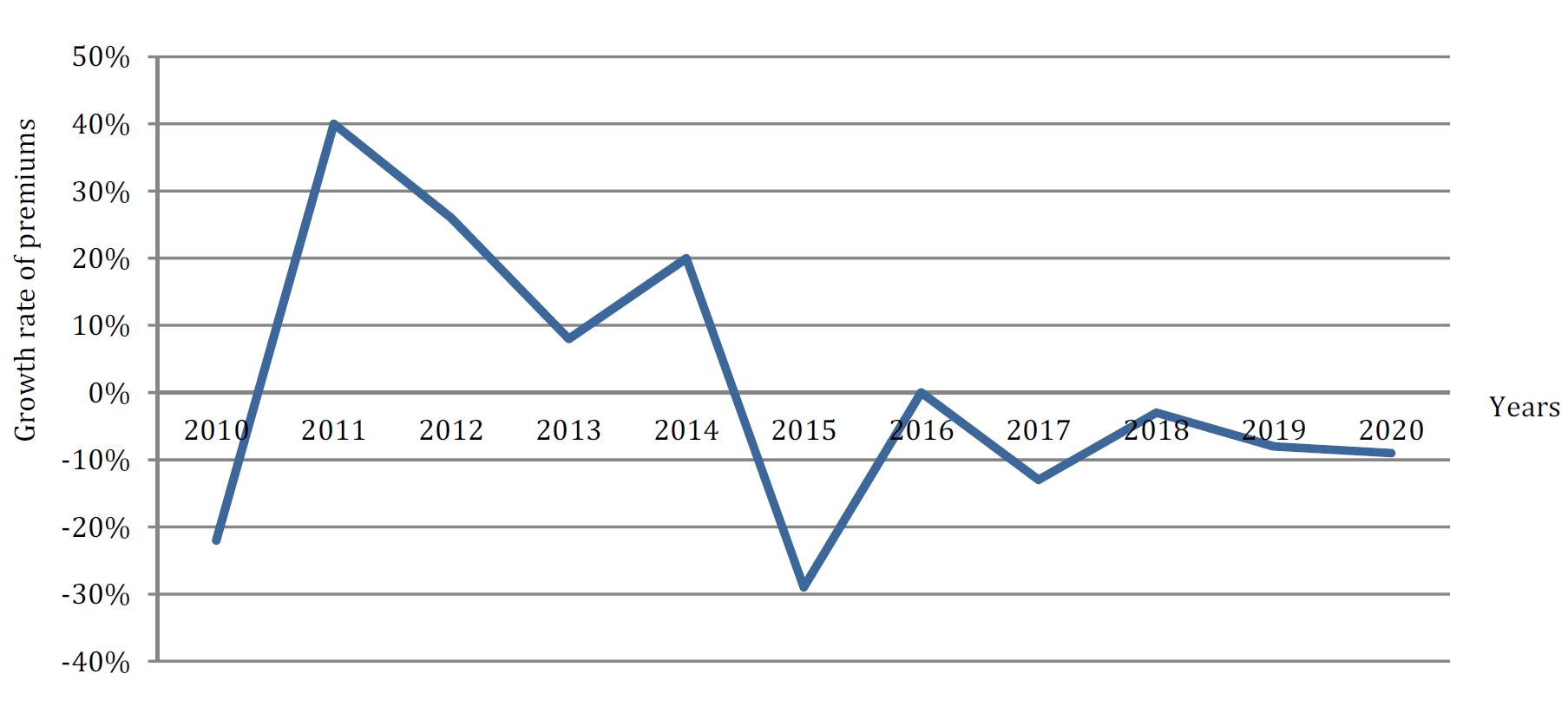

Growth rate of insurance premiums reinsurance company (2010-2020) (Table 3, Figure 4)

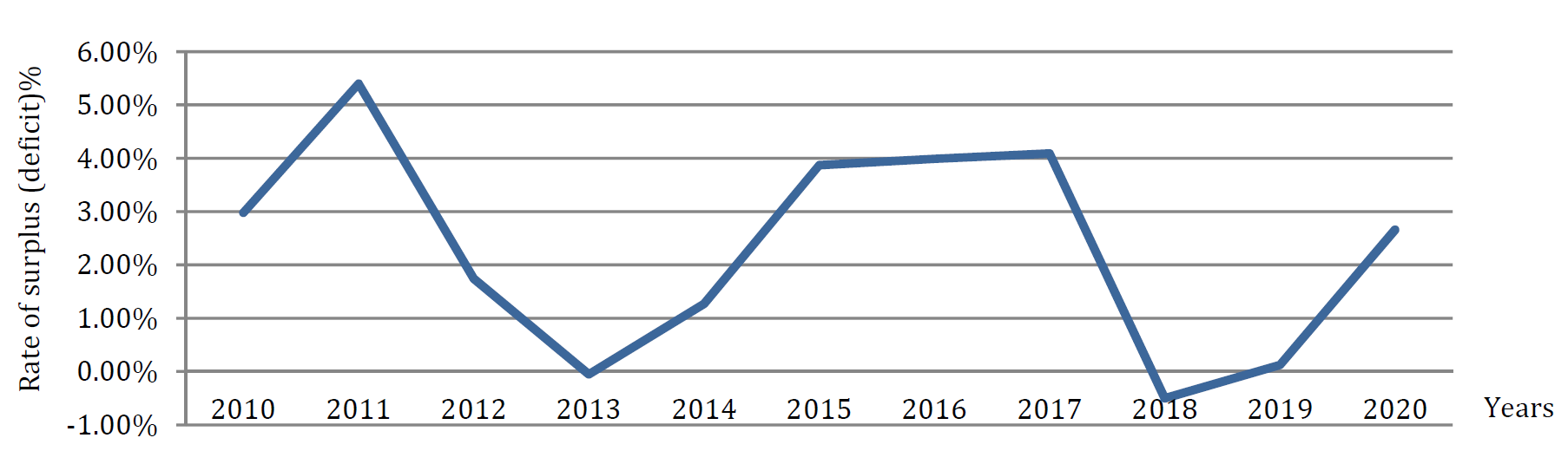

Growth rate in the surplus (deficit) of the company for the period (2010-2020) (Table 4, Figure 5)

The growth rate of compensation paid to the company for the period (2010-2020) (Table 5, Figure 6)

The growth rate of the reserves of the company for the period (2010-2020) (Table 6, Figure 7)

Growth rate of investment amounts of the company for the period (2010-2020) (Table 7, Figure 8)

The growth rate of investment revenues of the company for the period (2010-2020) (Table 8, Figure 9)

The Company’s profit growth rate for the period (2010-2020) (Table 9, Figure 10)

Table 1: Per Capita Productivity Growth Rate for the Company for the Period (2020-2010)

Year | Number of employees | Realized premiums | Per capita productivity | Growth rate in per capita productivity % |

2009 | 93 | 1.298E+10 | 139535144 | - |

2010 | 108 | 1.008E+10 | 93365166 | (33,09) |

2011 | 119 | 1.414E+10 | 118796397 | 27,24 |

2012 | 137 | 1.789E+10 | 130554707 | 9,90 |

2013 | 134 | 1.943E+10 | 144980295 | 11,05 |

2014 | 132 | 2.349E+10 | 177942518 | 22,74 |

2015 | 127 | 1.649E+10 | 129860743 | (27,02) |

2016 | 136 | 1.642E+10 | 120755390 | (7,01) |

2017 | 132 | 1.424E+10 | 107903673 | (10,64) |

2018 | 118 | 1.375E+10 | 116532042 | 8,00 |

2019 | 130 | 1.262E+10 | 97092018 | (16,68) |

2020 | 118 | 1.143E+10 | 96858310 | (0,24) |

Source: by the researcher based on the company's balance sheet and annual report for the period 2020-2010

Figure 2: Per Capita Productivity Growth Rate for the Company for the Period (2010-2020)

Figure 3: Percentage of Wage Productivity for the Company for the Period (2010-2020)

Figure 4: Growth Rate of Premiums Achieved by the Company for the Period (2010-2020)

Table 2: Wage Productivity of the Company for the Period (2020-2010)

Year | Realized premiums | Salaries and wages paid | Wage productivity % |

2010 | 1.01E+10 | 1.19E+09 | 8,47 |

2011 | 1.41E+10 | 1.37E+09 | 10,34 |

2012 | 1.79E+10 | 1.5E+09 | 11,92 |

2013 | 1.94E+10 | 1.59E+09 | 12,25 |

2014 | 2.35E+10 | 1.74E+09 | 13,46 |

2015 | 1.65E+10 | 1.77E+09 | 9,33 |

2016 | 1.64E+10 | 1.62E+09 | 10,16 |

2017 | 1.42E+10 | 1.57E+09 | 9,06 |

2018 | 1.38E+10 | 1.42E+09 | 9,67 |

2019 | 1.26E+10 | 1.39E+09 | 9,06 |

2020 | 1.14E+10 | 1.35E+09 | 8,45 |

Source: by the researcher based on the company's balance sheet and annual report for the period (2020-2010)

Table 3: The Growth Rate of Insurance Premiums for the Company for the Period (2020-2010)

Year | Realized Premiums | Realized Premiums Growth% |

2009 | 1.298E+10 | - |

2010 | 1.008E+10 | (22,30) |

2011 | 1.414E+10 | 40,20 |

2012 | 1.789E+10 | 26,52 |

2013 | 1.943E+10 | 8,62 |

2014 | 2.35E+10 | 20,90 |

2015 | 1.65E+10 | (29,79) |

2016 | 1.642E+10 | (0,42) |

2017 | 1.42E+10 | (13,27) |

2018 | 1.38E+10 | (3,46) |

2019 | 1.26E+10 | (8,21) |

2020 | 1.14E+10 | (9,45) |

Source: By the researcher based on the company's balance sheet and annual report for the period (2020-2010)

Figure 5: The Percentage of Surplus (Deficit) of the Company for the Period (2010-2020)

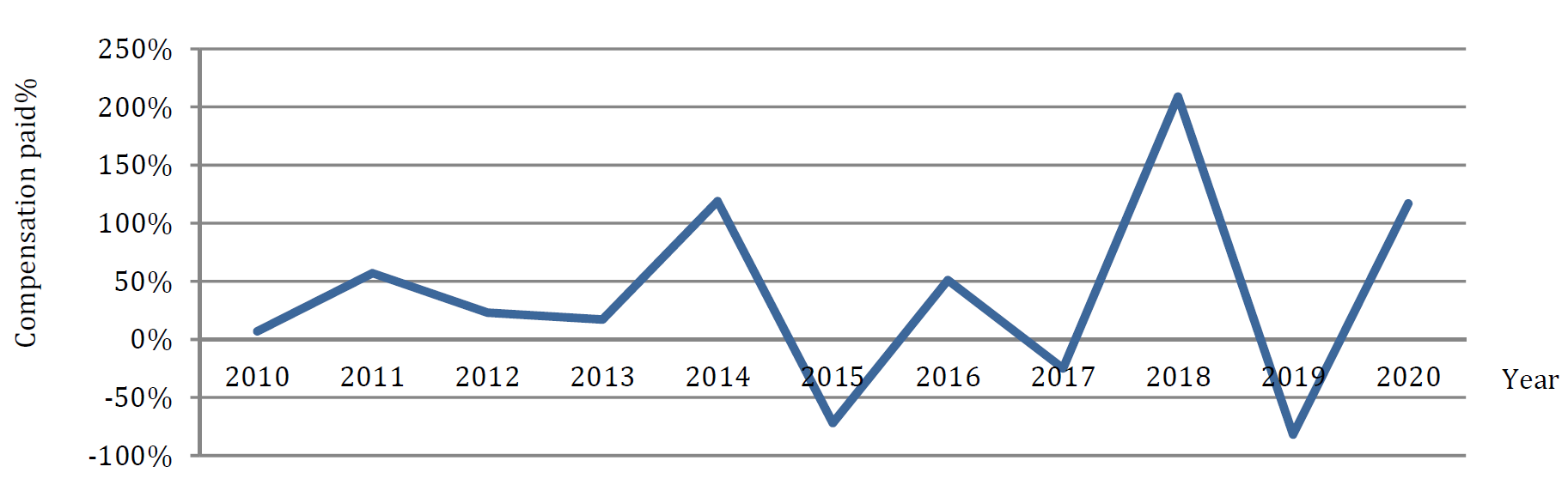

Figure 6: Growth Rate of Compensation Paid to the Company for the Period (2010-2020)

Table 4: Growth Rate in the Surplus (Deficit) of the Company for the Period (2010-2020)

Year | Revenues from insurance operations | Expenses from insurance operations | Surplus (deficit) | Rate of surplus (deficit) % |

2010 | 1.51E+10 | 1.46E+10 | 4.5E+08 | 2,98 |

2011 | 1.9E+10 | 1.8E+10 | 1.03E+09 | 5,40 |

2012 | 2.46E+10 | 2.42E+10 | 4.3E+08 | 1,74 |

2013 | 2.7E+10 | 2.7E+10 | -13883277 | (0,05) |

2014 | 3.13E+10 | 3.09E+10 | 3.98E+08 | 1,27 |

2015 | 2.28E+10 | 2.19E+10 | 8.84E+08 | 3,87 |

2016 | 2.32E+10 | 2.22E+10 | 9.25E+08 | 3,99 |

2017 | 2.43E+10 | 2.33E+10 | 9.95E+08 | 4,09 |

2018 | 2.45E+10 | 2.47E+10 | -121511305 | (0,50) |

2019 | 1.63E+10 | 1.63E+10 | 20392523 | 0,12 |

2020 | 1.7E+10 | 1.66E+10 | 4.53E+08 | 2,66 |

Table 5: Growth Rate of Compensation Paid to the Company for the Period (2010-2020)

Year | Compensation paid | Growth rate of compensation paid% |

2009 | 5.44E+08 | - |

2010 | 5.82E+08 | 7,05 |

2011 | 9.15E+08 | 57, 27 |

2012 | 1.13E+09 | 23,71 |

2013 | 1.33E+09 | 17,02 |

2014 | 2.91E+09 | 119,51 |

2015 | 7.9E+08 | (72,85) |

2016 | 1.19E+09 | 51,06 |

2017 | 8.84E+08 | (25,92) |

2018 | 2.73E+09 | 209,10 |

2019 | 4.79E+08 | (82,45) |

2020 | 1.04E+09 | 117,62 |

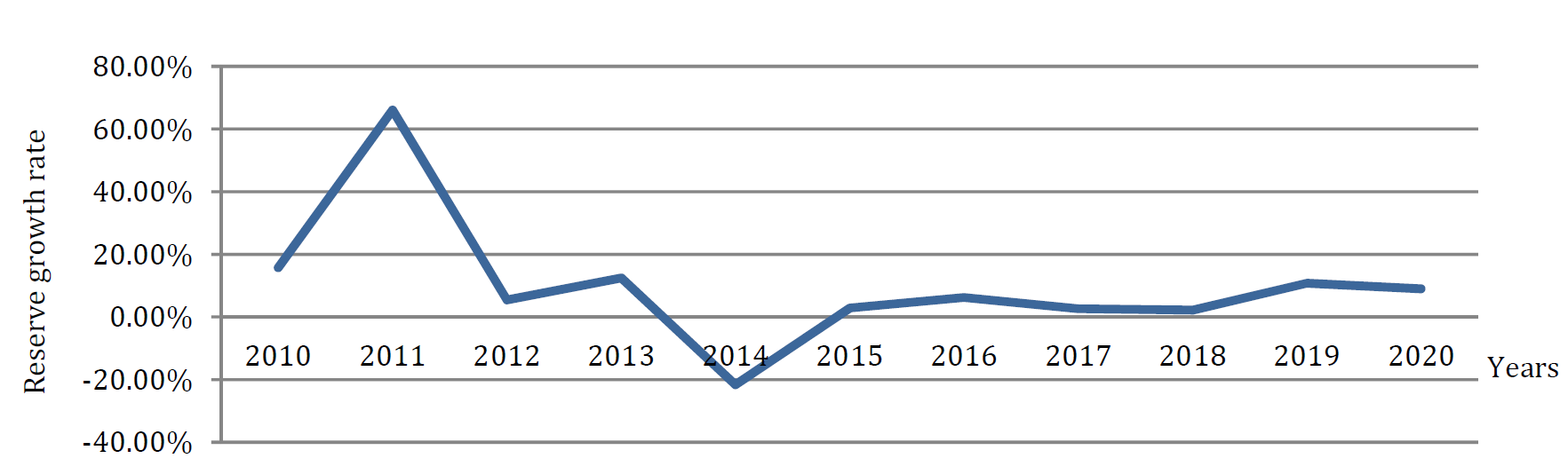

Table 6: Reserve Growth Rate of the Company for the Period (2010-2020)

Year | The reserves | Growth rate of the reserves% |

2009 | 1.67E+10 | - |

2010 | 1.93E+10 | 15,77 |

2011 | 3.2E+10 | 66,05 |

2012 | 3.38E+10 | 5,45 |

2013 | 3.8E+10 | 12,46 |

2014 | 2.98E+10 | (21,63) |

2015 | 3.06E+10 | 2,86 |

2016 | 3.25E+10 | 6,26 |

2017 | 3.34E+10 | 2,64 |

2018 | 3.41E+10 | 2,17 |

2019 | 3.78E+10 | 10,74 |

2020 | 4.12E+10 | 9,01 |

Figure 7: Reserve Growth Rate of the Company for the Period (2010-2020)

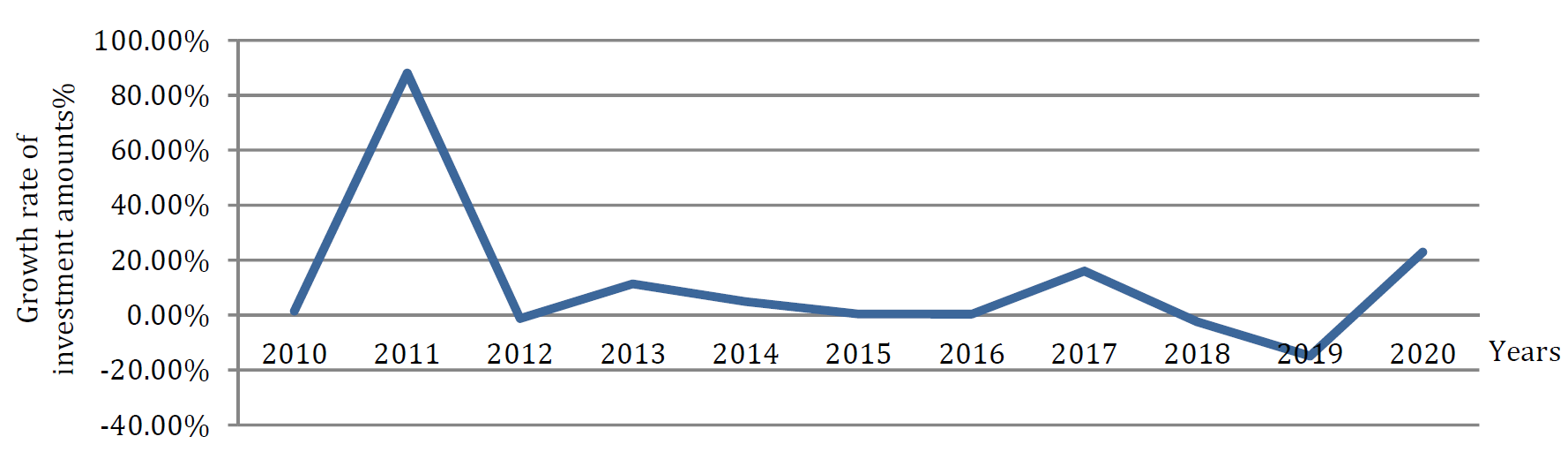

Figure 8: Growth Rate of Investment Amounts for the Company for the Period (2010-2020)

Table 7: Growth Rate of Investment Amounts for the Iraqi Company for the Period (2010-2020)

السنة | Investment amounts | Growth rate of investment amounts% |

2009 | 1.78E+10 | - |

2010 | 1.81E+10 | 1,47 |

2011 | 3.4E+10 | 88,03 |

2012 | 3.36E+10 | (1,29) |

2013 | 3.74E+10 | 11,33 |

2014 | 3.92E+10 | 4,91 |

2015 | 3.93E+10 | 0,36 |

2016 | 3.95E+10 | 0,35 |

2017 | 4.58E+10 | 16,03 |

2018 | 4.47E+10 | (2,44) |

2019 | 3.8E+10 | (14,87) |

2020 | 4.67E+10 | 22,90 |

Figure 8: Growth Rate of Investment Amounts for the Company for the Period (2010-2020)

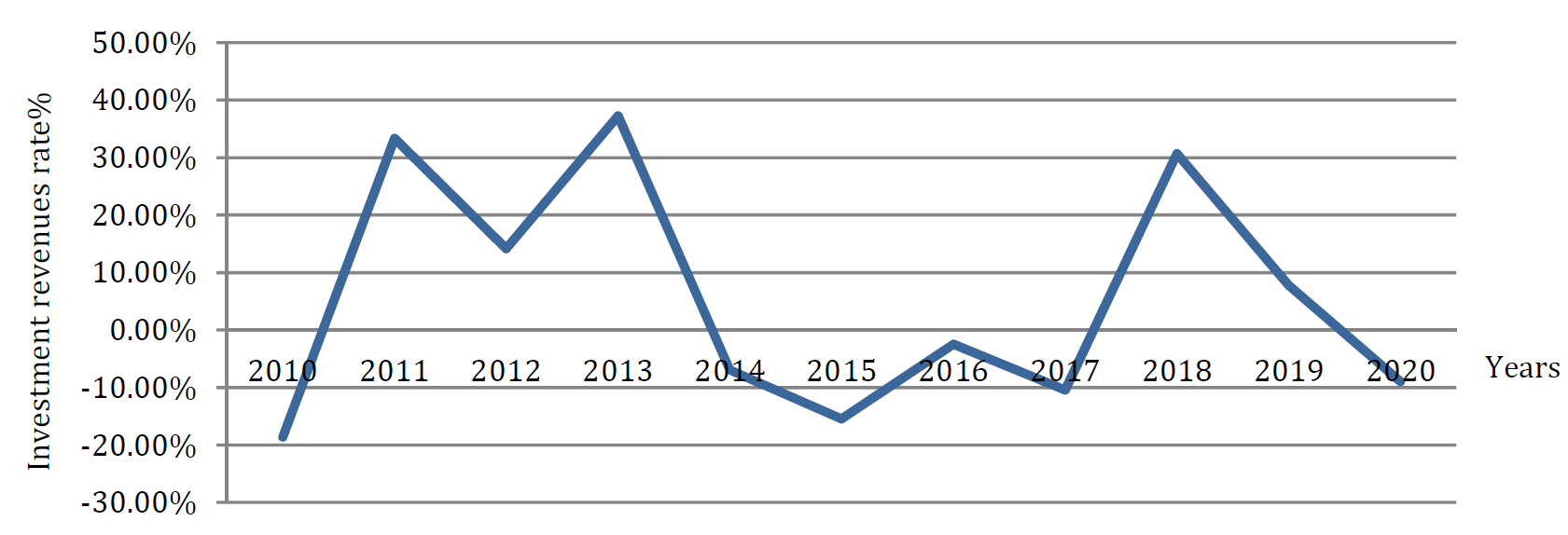

Year | Investment revenue | Investment revenue growth % |

2009 | 1.83E+09 | - |

2010 | 1.49E+09 | (18,61) |

2011 | 1.98E+09 | 33,31 |

2012 | 2.26E+09 | 14,14 |

2013 | 3.11E+09 | 37,27 |

2014 | 2.89E+09 | (6,92) |

2015 | 2.44E+09 | (15,45) |

2016 | 2.38E+09 | (2,46) |

2017 | 2.14E+09 | (10,42) |

2018 | 2.79E+09 | 30,69 |

2019 | 3.01E+09 | 7,78 |

2020 | 2.74E+09 | (8,95) |

Table 9: The Company’s Profit Growth Rate for the Period (2010-2020)

Year | Realized profits | Profit growth rate% |

2009 | 8.41E+08 | - |

2010 | 8.61E+08 | 2,39 |

2011 | 1.05E+09 | 22,13 |

2012 | 8.24E+08 | (21,62) |

2013 | 1.01E+09 | 22,58 |

2014 | 1.15E+09 | 14,10 |

2015 | 1.2E+09 | 3,77 |

2016 | 1.23E+09 | 2,79 |

2017 | 1.24E+09 | 0,56 |

2018 | 1.27E+09 | 2,85 |

2019 | 1.55E+09 | 21,90 |

2020 | 1.6E+09 | 3,27 |

Figure 9: The Growth Rate of Investment Revenues of the Company for the Period (2010-2020)

Based on what was discussed in the theoretical side of the research and what was reached in the practical side, the researcher reached a set of results, we mention them sequentially: It was noticed that there was a weakness in the financial performance of the company, especially in the recent years of the research, the most important of which was the decline in the growth rate of reinsurance premiums, which represents the main activity of the company, in addition to stopping work in the reinsurance activity of the life insurance portfolio starting from the year 2019. With regard to liquidity, the company has liquidity that makes it able to pay its obligations, especially in the period (202-2019). 0), as for profitability, it was noted that there is a fluctuation in the rate of return on investment starting from 2011 to 2017, with an increase in this rate for the years 2018-2020, which indicates an increase in the company’s profits and its total assets and its ability to operate those assets and achieve profits.

It was also noted that the company suffers from a decrease in per capita productivity from the earned premiums and the company achieved only slight progress during the years 2011 and 2014.

The company suffers from a decrease in the number of employees working in it due to the referral of many of them to retirement due to their reaching the legal age or because of their transfer or placement to other departments, which caused a shortage of qualified employees with experience in the company in a way that covers the actual need of the company and poor planning for that.

It was also noticed a decrease in the indicator of the development of insurance premiums, as it reached the lowest percentage in 2015, when it amounted to (29.79%), due to the events of ISIS entering Iraq and the cessation of many engineering projects, in addition to the practice of some insurance companies in reinsurance business.

The company achieved the highest surplus growth rate in 2011 and the lowest surplus rate in 2019, with a deficit emerging in the years (2013 and 2018). While the growth rate of compensation paid by the company increased due to poor study of reinsurance policies and the acceptance of high-risk policies.

It was also noted a decrease in the growth rate of the company's reserves during the period under study due to the decrease in its profits and its inability to increase its reserves. It was also found through the analysis of the indicator of the development of the investment amounts of the company, the decrease in investment revenues due to the lack of direction towards expanding the investment outlets, including the purchase of stocks and bonds and trading in the Iraqi stock market. It was also shown by following up on the company’s profits that there was a sharp decline for the year 2020, which amounted to (2.27%) compared to the year 2019, when it reached (21.90%), which indicates the poor financial performance of the company in general and thus the research hypothesis is fulfilled.

Bahr, Saba Adnan. Evaluating the Performance of the Iraqi Insurance Company. Higher diploma research, University of Baghdad, 2020.

Muhammad, Faiza Abdul-Karim. “Evaluating the Financial Performance of the Iraqi Insurance Company.” Journal of Financial and Accounting Studies, vol. 8, no. 22, 2013.

Al Dalayeen, Basman. “Financial Performance Appraisal of Selected Companies in Jordan.” Open Journal of Business and Management, vol. 5, 2017.

Hassan, Rafah and Mona Bitar. “Factors Affecting the Financial Performance of Private Insurance Companies Operating in Syria.” Journal of Economic and Financial Research, vol. 7, no. 2, 2020.

Sabah, Zroukhy et al. “The Importance of Studying Financial and Technical Indicators for Insurance Companies in Algeria: A Case Study of the State of M’sila.” Journal of Research in Financial and Accounting Sciences, vol. 3, no. 1, 2018.

Abu Madi and Kamel Ahmed. The Balanced Scorecard as a Tool for Evaluation of the Performance of Governmental and Non-Governmental Institutions. Nissan Bookstore for Printing and Distribution, 2018.

Abd Al-Rahim, Ainoush and Dahmani Abd Al-Wafi. Assessment of Financial Performance in Insurance Companies: An Applied Study in the Regional Fund for Agricultural Cooperation 2016-2018. Master’s thesis, University of Bouira, 2019.

Al-Tarawneh, Anas Musleh Diab. Factors Affecting the Evaluation of the Financial Performance of Jordanian Insurance Companies: An Applied Study on Insurance Companies Listed on the Amman Stock Exchange. Master’s thesis, Middle East University, 2015.

Somaya, Haj Issa. Evaluating the Financial Performance of the Economic Institution Using the Benchmarking Mechanism: Case Study of Al-Safaa Filter Foundation and Al-Safi Filter Foundation. Master’s thesis, Larbi Ben M’hidi University, 2014.

Swanson, Richard and Elwood Holton. Management by Results: How to Measure the Level of Performance, Learning and Opinion within Institutions. 1st Ed., Dar Al-Farouk for Cultural Investments, 2010.

Fatihudin, Didin et al. “How Measuring Financial Performance.” International Journal of Civil Engineering and Technology, vol. 9, no. 6, 2018.

Nafisa, Hajjaj. The Impact of Investment in Information and Communication Technology on Financial Performance: A Case Study of a Sample of Algerian Petroleum Companies during the Period (2010-2014). PhD thesis, Kasdi Merbah University, 2017.

Dufera, Abidi. Financial Performance Evaluation: A Case Study of Awash International Bank (AIB). Master’s thesis, Mekelle University, 2011.

Mohamed, Abdullah Mohamed. “Evaluating the Financial Performance of Sudanese Insurance Companies According to Financial Solvency Standards.” Journal of Economic and Administrative Sciences, vol. 19, no. 1, 2018.

Katea, Hala Nasser. Reinsurance and Its Impact on the Financial Surplus of the National Insurance Company: Applied Research in the Marine Insurance Branch. Higher diploma research, University of Baghdad, 2020.

Mokhtari, Zahra. Financial Diagnosis and Its Role in Evaluating Performance in the Insurance Company: Case Study of the Algerian Insurance and Reinsurance Company during the Period (2005-2007). Master’s thesis, University of Mohamed Boukara Boumerdes, 2011.

Al-Anbaki, Shihab Ahmed Jassim. General Principles of Insurance. 2nd Ed., Thaer Al-Assami Foundation for Printing, Publishing and Distribution, 2022.

Katea, Hala Nasser and Alaa Abdel-Karim Al-Baldawi. “Reinsurance Risks and Their Impact on the Financial Performance of the National Insurance Company: Applied Research in the Marine Insurance Branch.” Journal of Financial and Accounting Studies, 2019.

Ray, Hodgin. Insurance Law: Text and Material. 2nd ed., Cavendish Publishing Limited, 2018.

Al-Wardi, Salim Ali. Al-Wajeez in General Reinsurance. 4th ed., Al-Adeeb Al-Baghdadiya Press Limited, 1987.

Kazem, Ansam Jaafar. Reinsurance and Its Impact on the Development of the Insurance Industry: A Comparative Study between the National Insurance Company and the Iraqi Insurance Company. Higher diploma research, University of Baghdad, 2010.