+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

This study aims to analyze and measure the impact of the change in the exchange rate on agricultural exports in Iraq in the period 1990-2022. Because this period has witnessed many changes and economic crises in Iraq, using the Autoregressive Distributed Lag Model-ARDL in estimation and analysis, so that the research reaches a set of results, the most important of which is that the error correction period was negative and significant value of about -0.63, i.e. approximately 18 months, during which errors or shocks that occur on the model and return it to the original equilibrium position. In addition to the absence of a long-term relationship to the lack of significance of the exchange rate in the long-term model, the results proved the existence of joint integration between the two variables and the research recommended avoiding obstacles that affect the volume of exports and reduce their impact by diversifying exports and searching for new markets, improving the quality of exported products, improving infrastructure and taking measures to improve the economic environment.

International trade is based on a fixed base which is export and import and if it is conceivable that a country imports more than it exports or exports more than it imports, it is rare-although not impossible-that there is a country outside this cycle (that is, completely self-sufficient) and with the high rates of trade and the multiplicity of currencies in circulation, it requires a mechanism through which each of the currencies in circulation is evaluated against the rest of the currencies, as this mechanism is called the exchange rate, The exchange rate is one of the important economic variables due to the extent of its contribution to achieving economic goals and achieving external balance at the level of the balance of payments, so the balance of trade through exports and imports is important to maintain the safety of the local economy from economic crises.

There is a close relationship between the exchange rate and the trade balance of any country. The correlation is that the exchange rate affects the volume of exports and imports and then the trade balance, when the price of the local currency falls, the local product becomes cheaper for foreign buyers, which increases the volume of exports and reduces the volume of imports, that is, the devaluation of the national currency allows the country to export more and the foreign currency rises again [1]. This ultimately leads to a surplus in a country's trade balance and exchange rate changes trigger changes in domestic goods relative to prices in foreign countries, affecting exports [2]. On the other hand, when the price of the local currency rises, the imported product becomes cheaper for domestic buyers, which increases the volume of imports and reduces the volume of exports. This ultimately leads to a reduction in the trade balance surplus or an increase in a country's trade balance deficit.

Under the influence of J-curve, real exchange rate depreciation is often synonymous with a deterioration in a particular country's trade balance in the short term, because most import and export orders are submitted several months in advance. The value of the level of pre-contracted imports in terms of domestic products rises, which means that there is an initial decline in the current account, to increase their sales abroad, exporters may need to adjust their ability to reach foreign consumers. Which may also take time. In the long run, when these adjustments occur, real exchange rate depreciation may improve the current account [3].

Agricultural export is one of the sources of obtaining the necessary foreign exchange to finance the import of modern agricultural technologies, reduce the deficit in the agricultural trade balance, ensure the continuity of presence in foreign markets, especially traditional ones, as well as the ability to compete to maintain market share or try to increase it [4]. Therefore, agricultural export activity is one of the means of achieving increasing rates of agricultural growth. The importance of export for developing countries stems from the reality of structural imbalances that it is noted that the trade balance deficit worsens, the volume of external indebtedness increases, its burdens increase and thus its import capabilities weaken, due to the policies pursued by some developing countries, such as the import substitution policy and the external lending policy, so export is an important decision that can be relied upon to provide the needs of foreign exchange in an orderly manner, especially since other sources (exports of raw materials) are not characterized by stability and continuity [5]. The process by which goods and services flow from the national territory and are diverted beyond borders and can be in abundance or a few". The importance of exchange rate stability is the direct impact of exchange rates on import prices and stability in exchange rates attracts investors as a result of price stability within the country [6]. The trade balance in Iraq has one sector in which its role stands out and determines the movement within the balance, which is the oil sector and therefore the trade balance without the oil sector suffers from a permanent deficit due to dependence on it almost completely. Therefore, the importance of the research comes from the importance of changing the exchange rate on some economic variables (exports and agricultural imports), especially since the reflection of that impact is directly or indirectly on those variables, which is reflected in the motivation of the Iraqi economy, in addition to the role of the exchange rate in the balance of the trade balance, which is one of the most important economic indicators and a tool of economic analysis tools to know the economic situation of a country. Agricultural exports are also a source of foreign exchange in parallel with the growth of imports of investment goods necessary for national development plans to increase capital accumulation and establish the industrial base, so the research problem revolves around understanding the relationship between the two variables and the basic factors that affect them and identifying the appropriate tools to analyze them accurately and understand them better, especially since some economic theories indicate pointed out that exchange rate movements can affect the volume of exports. By knowing the nature of the relationship between the exchange rate and exports (outside hydrocarbons), it becomes clear the relative importance of foreign trade, especially since the Iraqi economy is a rentier economy dependent on the export of oil by a large percentage, as foreign currency exchange rates affect the trade balance of agricultural goods. Hence, the objective of the research is identifying the reality of Iraq in terms of the development of the structure of agricultural exports and the exchange rate and highlight the most important joints of these variables during the period studied. Estimating and analyzing the impact of the exchange rate on agricultural exports and its differentiated effects on it and formulating a comprehensive mathematical model to identify the short- and long-term relationships between them. For this purpose, the time series data covering the period from 1990 to 2022, obtained from government agencies such as the Central Bank and the FAO website, was used, while the analysis method was used ARDL model with the help of the statistical program Eviews 12.

Agricultural Exports in Iraq for 1990-2022

Exports are a reflection of the available domestic production capacities, as well as an indicator of the expansion of the domestic production base and a factor to reveal the possibility of diversifying it and playing an important role in covering imports and reducing the burden of external debt through the foreign currency they bring [7]. Exports are one of the important indicators to measure the volume and level of foreign trade, the higher its percentage, the more positive its reflection on the trade balance, as exports represent an element of flow of income, as they add new purchasing power to the current of total monetary spending and that exports are the only financier of the country of foreign currency through which spending on all other economic sectors is made, under exports the state can discharge its surpluses from domestic production, Despite the role played by exports in achieving economic growth and thus economic development, the commodity structure of exports in Iraq is a stable structure, as it depends mainly on oil exports and products, in other words, Iraq faces a dilemma that concentrates its commodity exports, as it depends largely on the export of mineral fuels without other commodities and these percentages may indicate that the Iraqi economy is infected with complications of the Dutch disease [8]. The growth rate of agricultural exports in Iraq during the period studied was 0.08%, reflecting the relative decline despite the improvement in exports in some years and the values ranged from a minimum of approximately $ 4.71 million in 1993 due to the economic sanctions imposed on the country at the time, to an upper limit of $ 351.42 billion in 2004, due to the openness to the world after the war in 2003 and the expansion of the use of the benefits of the Generalized System of Preferences - GSP, which provides an exemption from customs duties for 3400 types of Iraqi goods (exports) to the USA and Iraq joined it in September 2004, gives Iraqi exports an advantage in the American market that these exports do not impose tariffs on them and therefore their cost is lower for American importers Iraqi exports to the United States of America, as exports, in general, increased during the post-war period due to the lifting of all restrictions (Figure 1).

Figure 1: Agricultural Exports and Exchange Rates in Iraq for 1990-2022

Resources: By researchers based on data from the Central Bank and FAO statistics

Table 1: Unit Root Test PP Criteria

| XP | EX | d(XP) | d(EX) | |

With Constant | t-Statistic | -3.3105 | -2.4405 | -21.2995 | -6.0335 |

Prob. | 0.0227 | 0.1392 | 0.0001 | 0.0000 | |

| ** | No | *** | *** | |

With Constant & Trend | t-Statistic | -4.6475 | -2.0148 | -20.5600 | -6.4043 |

Prob. | 0.0040 | 0.5714 | 0.0000 | 0.0000 | |

|

| *** | No | *** | *** |

Without Constant and Trend | t-Statistic | -1.6036 | -0.2519 | -13.6700 | -6.0100 |

Prob. | 0.1013 | 0.5875 | 0.0000 | 0.0000 | |

| No | No | *** | *** | |

*Significant at 10%, significant at 5%, ***Significant at 1%, No: Non-significant, Resource: Researchers using Eviews 12

Time Series Stationary Test

A test was conducted for the stability of time series and Table 1 shows the test results for the studied economic variables, to verify the level at which the data stabilize and the Phillips-Perron (PP) test for stationary was adopted and is more accurate for the results of the data in small samples [9] and we note the stability of the data for the variables when taking the first difference to them and at a significant level of 1%.

Autoregressive Distributed Lag-ARDL

The time series, whether dependent or independent variables are affected by their lagged periods and the ARDL model can be applied to stable variables of the same rank, whether I(0) or I(1), or different ranks, provided that they are not of the order I(2), which is a developed model for the Error Correction Model - ECM, which when applied is assumed that the variables are integrated of the same degree, noting that the short-term relationship between variables is estimated as well as the cointegration is implicitly extracted according to the Wald Test or the so-called Bound Test, which is concerned with proving or denying the long-term relationship between variables [10] and the relationship will be estimated using the ARDL model:

where, XP value of agricultural exports in million dollars (dependent variable), EX exchange rate of the Iraqi dinar against US dollar (independent variable), k number of lags βi’s short-term parameters φi’s long-term parameters and εi random error.

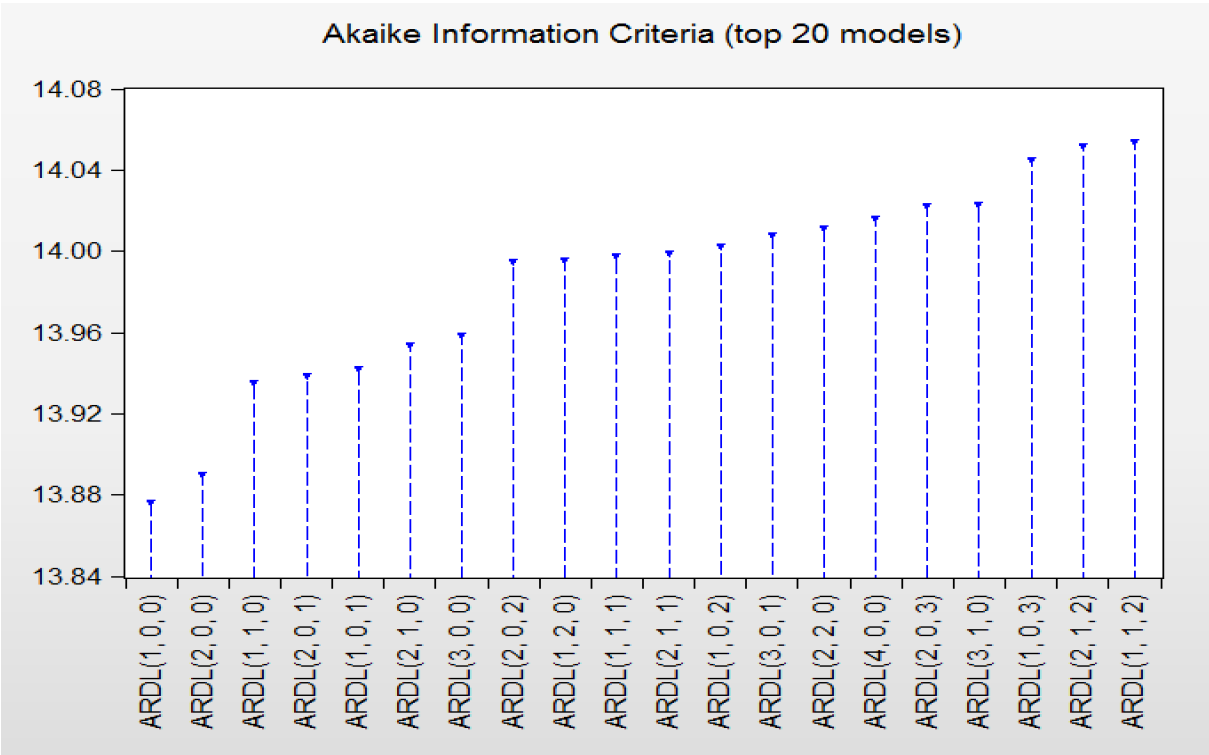

Table 2 shows the results of the estimation of the effect of independent variables with their slowdown periods on the dependent variable, as well as the effect of slowing down periods of the dependent variable itself and the results showed the choice of formula (1,1), which is the best result obtained, which suffers from one slowdown for the dependent variable XP and a slowdown for the second independent variable EX (Figure 2).

Analysis and Testing of the ARDL Model

Normal Distribution Test: It is a statistical test concerned with the normal distribution of the chain, the test statistic measures the difference in the torsion and hyperbolism of the chain with those in the normal distribution and it is calculated as follows:

where, S: Skewness, K: Kurtosis.

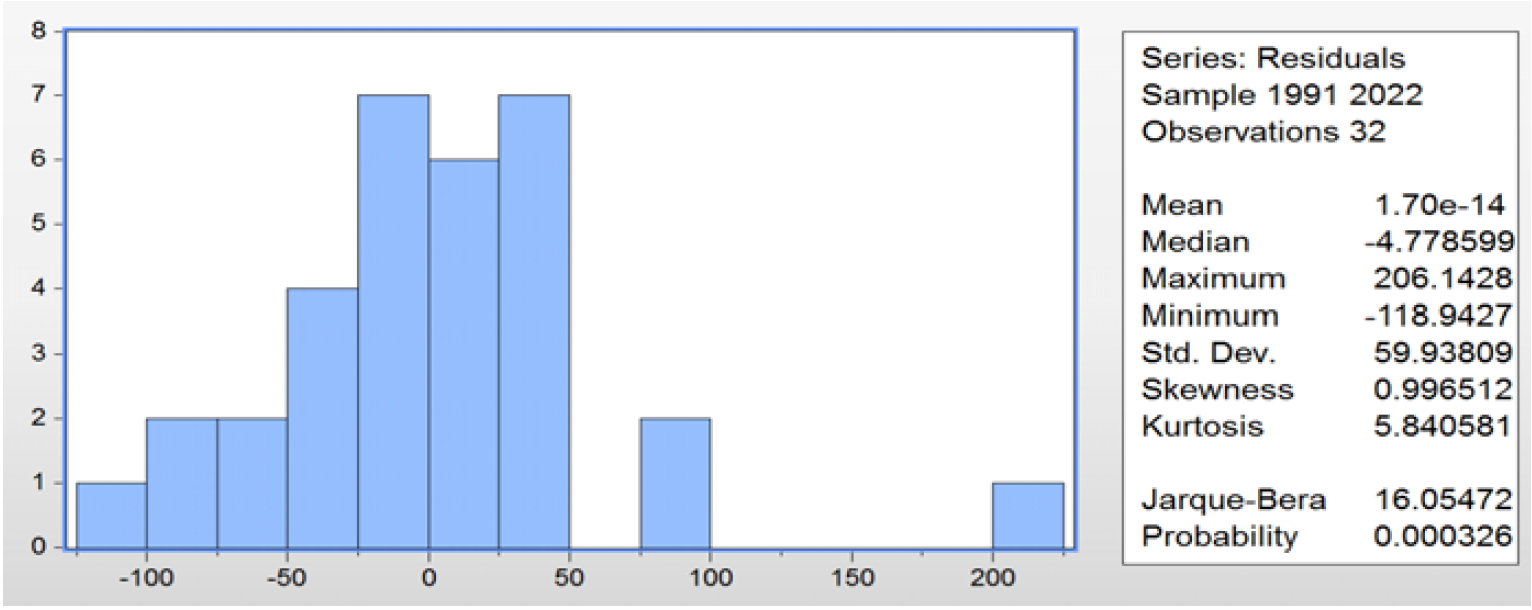

Under the null hypothesis of the normal distribution, the Jarque-Bera statistic follows the chi-square distribution χ2 with 2 degrees of freedom and the resulting probability is the probability that the Jarque-Bera statistic exceeds (in absolute terms) the observed value, the small probability value rejects the null hypothesis of the normal distribution and accepts the alternative and therefore the variable is not distributed normally. Figure 3 and the table attached to it show the insignificance of the Jarque-Bera test, which reached 16.05, which means acceptance of the null hypothesis that states the normal distribution of the estimated ARDL model remainder series.

Figure 2: The Best Results Obtained Involve the Application of the ARDL Model

Resource: Researchers using Eviews 12

Figure 3: Test of the Normal Distribution of Residues According to the Jarque-Bera Standard

Resource: By Authors Using Eviews 12

Table 2: Estimated ARDL Model

Sample (adjusted): 1991 2022 | ||||

Included observations: 32 after adjustments | ||||

Maximum dependent lags: 4 (Automatic selection) | ||||

Model selection method: Akaike info criterion (AIC) | ||||

Dynamic regressors (4 lags, automatic): EX | ||||

Number of models evaluated: 20 | ||||

Selected Model: ARDL (1, 1) | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob.* |

XP (-1) | 0.362659 | 0.162437 | 2.232608 | 0.0338 |

EX | -0.050478 | 0.043916 | -1.149424 | 0.2601 |

EX (-1) | 0.081169 | 0.040970 | 1.981192 | 0.0575 |

C | 21.83653 | 31.99214 | 0.682559 | 0.5005 |

R-squared | 0.325020 | Mean dependent var | 88.36838 | |

Adjusted R-squared | 0.252701 | S.D. dependent var | 72.95540 | |

S.E. of regression | 63.06738 | Akaike info criterion | 11.24275 | |

Sum squared resid | 111369.8 | Schwarz criterion | 11.42597 | |

Log-likelihood | -175.8840 | Hannan-Quinn criter. | 11.30348 | |

F-statistic | 4.494234 | Durbin-Watson stat | 2.123686 | |

Prob(F-statistic) | 0.010725 |

| ||

Source: Researchers using Eviews 12

Breusch-Godfrey Serial Correlation Test

An important test in this area is the sequential autocorrelation test for model error limit using the Serial Correlation LM Test developed by Breusch and Godfrey in 1978. The results are shown in Table 3. The lack of autocorrelation under the results of the LM test by comparing the Chi-Square statistical probability of 0.74, which is greater than 0.05 and therefore we accept the null hypothesis, meaning that the model is good and there is no sequential self-correlation in errors.

Figure 4: CUSUM and CUSUMSQ Stability Tests for the Estimated Model

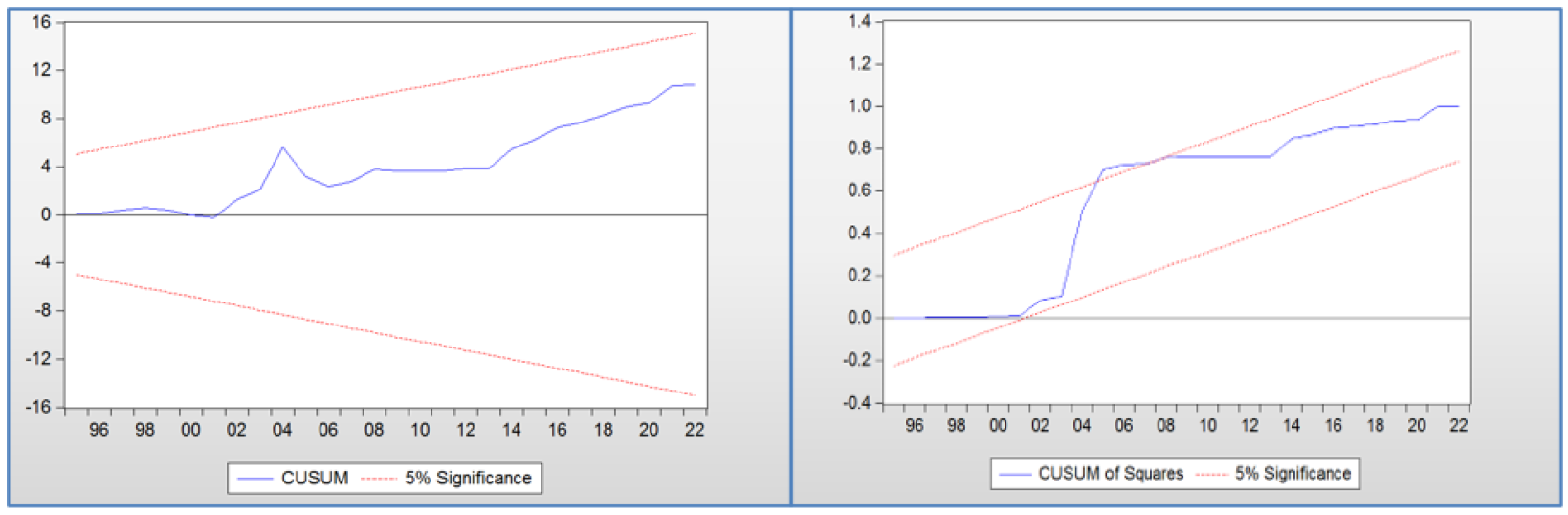

Resource: By Authors Using Eviews 12

Table 3: Lagrange LM Multiplier Test

Breusch-Godfrey Serial Correlation LM Test: |

| ||

F-statistic | 0.248734 | Prob. F (2,26) | 0.7816 |

Obs*R-squared | 0.600773 | Prob. Chi-Square (2) | 0.7405 |

Resource: By Authors Using Eviews 12

Table 4: Heteroscedasticity Test: Breusch-Pagan-Godfrey

F-statistic | 1.854730 | Prob. F (3,28) | 0.1602 |

Obs*R-squared | 5.304882 | Prob. Chi-Square (3) | 0.1508 |

Resource: By Authors Using Eviews 12

Table 5: Short-Run Model (Error Correction)

Sample: 1990 2022 | ||||

Included observations: 32 | ||||

ECM Regression | ||||

Case 2: Restricted Constant and No Trend | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

D (EX) | -0.050478 | 0.037935 | -1.330649 | 0.1940 |

CointEq (-1) | -0.637341 | 0.151727 | -4.200588 | 0.0002 |

Resource: By Authors Using Eviews 12

Heteroscedasticity Test

Based on the Breusch-Pagan-Godfrey test (BPG), the calculated F-value of (1.85) was obtained and its significance was 0.16 and the results of the variance test conducted on the model confirmed that the Chi-Square statistical value reached 0.15, which is greater than 0.05 as well and therefore there is no difference in variance in the error limit and then accept the null hypothesis, i.e. no problem, as in Table 4.

CUSUM and CUSUMSQ Testes

The structural stability of the estimated ARDL model coefficients (1.1) is achieved if the graph of the statistics of both CUSUM and CUSUMSQ falls within the critical limits at a significant level of 5% and these coefficients are unstable if the graph of the statistics of the two tests mentioned moves outside the boundaries at this level. The results showed structural stability between the two variables of the study and harmony in the model in the short and long term (Figure 4).

Error Correction Model ECM

The following short-term model (error correction) was applied to the estimate:

where, k number of slowdowns βi’s short-term parameters of the error correction model, εi random error.

What matters is that the error correction coefficient CointEq (-1) appears significantly as a necessary condition and negative as a sufficient condition, as a negative signal means that there is a co-integration relationship and that there is the possibility of correcting short-term errors to return to the long-term equilibrium position and that the absolute value of this estimate is the percentage of errors that can be treated per unit time, meaning if a shock occurs, in each unit of time (year) this percentage of error can be treated [11].

The results of Table 5 show that the value of the error correction coefficient was -0.63, which is significant at 1% and it explains that the treatment of shock (or short-term deviation) occurring in this model requires more than a year and a half to return to normal because 0.63% of the effects of the shock are treated in one year, as the period required to correct the impact of the shock and return to the correct position is equal to the reciprocal of this ratio, i.e., (1/0.63) = 1.5 years, i.e. approximately 18 months, that is, the error correction model represents the short-term model, in which errors or shocks that occur in the model are corrected and returned to the original equilibrium position.

Long-Run Function and Boundary Test

They appear in this estimate as in Table 6. The estimate of the export variable last year was negative and significant at 1%, which means the change in global demand for products exported by the country, which leads to a decline in the value of exports in the current year, the exchange rate was positive and insignificant, meaning that there is no long-term relationship between agricultural exports and the exchange rate and there is no long-term relationship for exports on the other hand.

The bound-test for the model as a whole can be deduced by comparing the F statistic with the lower and upper limits, as in Table 7. If the statistic is greater than the upper limit and according to the level of significance, there is a common integration between the variables (the relationship of levels equation) and if the value of the F statistic is less than the minimum at the level concerned, this means accepting the hypothesis of nothingness and the absence of a relationship of joint integration, but in the case that the statistic F is located between the two limits, it means that the decision is not decisive and returning to the result of the F test amounted to 5.48 is greater From the upper limit at the 5% level to the lower limit at the 5% level, this means that there is a joint complementarity between the two variables.

Table 6: ARDL Long Run Form and Bounds Test

Dependent Variable: D (XP) | ||||

Selected Model: ARDL (1, 1) | ||||

Case 2: Restricted Constant and No Trend Sample: 1990 2022 | ||||

Included observations: 32 | ||||

Conditional Error Correction Regression | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | 21.83653 | 31.99214 | 0.682559 | 0.5005 |

XP (-1)* | -0.637341 | 0.162437 | -3.923613 | 0.0005 |

EX (-1) | 0.030691 | 0.022415 | 1.369209 | 0.1818 |

D(EX) | -0.050478 | 0.043916 | -1.149424 | 0.2601 |

Levels Equation | ||||

Case 2: Restricted Constant and No Trend | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

EX | 0.048155 | 0.036127 | 1.332926 | 0.1933 |

C | 34.26191 | 47.67357 | 0.718677 | 0.4783 |

EC = XP - (0.0482*EX + 34.2619) |

| |||

Resource: By Authors Using Eviews 12

Table 7: Boundary Test for the Estimated Model

F-Bounds Test | Null Hypothesis: No levels relationship | |||

Test Statistic | Value | Signif. | I(0) | I(1) |

|

| Asymptotic: n=1000 | ||

F-statistic | 5.489536 | 10% | 3.02 | 3.51 |

k | 1 | 5% | 3.62 | 4.16 |

|

| 2.5% | 4.18 | 4.79 |

|

| 1% | 4.94 | 5.58 |

Resource: Eviews 12 software output

The results of the Histogram-normality test for the ARDL model proved that the residues are distributed normally and the results of the Serial Correlation LM test indicated that there is no self-correlation between random residues and the Heteroskedasticity test proved that there is no problem of homogeneity of variance and that the model successfully passes the standard problems and is free of those problems to indicate the efficiency of the model and enhances the possibility of adopting its results in analysis, forecasting and policy-making

The absence of a long-term relationship between the exchange rate and exports can be due to several reasons, including that the monetary policy of successive governments in fixing the exchange rate has made it not change significantly and therefore does not affect the value of exports. Among them are changes in the supply and demand of exports greater than the exchange rate, as well as the impact of internal and external factors of the country on the volume of exports such as government policies, economic and social conditions and international trade relations. Therefore, these factors can have a greater impact on exports than the exchange rate

The reason for the decline in agricultural exports in Iraq during the research period as a result of the weakness of technical and modern methods, the high production costs and the accompanying lack and quality problems in the available products (in dates in particular), which reduces the competitiveness of local exports compared to global exports, as well as the apparent weakness of Iraqi marketers in the field of international marketing of agricultural products

Recommendations

Reconsider the policy of determining the exchange rate of the local currency against the dollar, taking into account the negative impact of the exchange rate reduction on food security, so it is necessary to conduct a balance between the objectives of macroeconomic policy and to adopt a comprehensive national strategy to maintain the stability (not control) of the exchange rate and make it appropriate and effective in the service of promoting and developing agricultural exports and the use of external capital in the development of the agricultural sector

Paying attention to the development of agricultural exports to Iraq, especially the important ones and making structural changes in them by converting them into value-added products. As well as diversification in exports, as export products can be diversified to include a variety of products and this helps to reduce the negative impact of any changes in global demand or changes in commodity prices

Searching for new markets for exports and expanding trade relations with other countries and this helps to reduce the negative impact of any changes in global demand or changes in commodity prices in some markets, as well as raising the level of quality, as the quality of exported products can be improved and quality requirements in global markets can be met. This helps to increase the demand for exported products and improve the country's reputation as a supplier of high-quality products

Make decisions to improve the economic environment in the country, such as improving the regulatory environment, reducing bureaucracy and providing support to exporting companies. This helps to encourage foreign investments and improve the business environment in the country

Beloufa, I. and A. Qadri. “The Impact of Algerian Dinar Exchange Rate Changes on the Trade Balance: An Econometric Study for 2000-2019.” Journal of Innovation and Marketing, vol. 10, no. 1, 2023, pp. 154-171.

Hadi, H.S. The Impact of the Exchange Rate on Some Macroeconomic Variables in Iraq. M.Sc. thesis, University of Karbala, College of Administration and Economics, 2022, pp. 25.

Auboin, M. and M. Ruta. “The Relationship between Exchange Rates and International Trade: A Review of Economic Literature.” WTO Staff Working Paper, no. ERSD-2011-17, World Trade Organization, 2011. https://doi. org/10.30875/13e83562-en.

oManea, S. and M. Haddad. “The Impact of the Change in the Exchange Rate of the Algerian Dinar on the Trade Balance.” Journal of Economic and Financial Studies, vol. 11, no. 1, 2018, pp. 210-221.

Ben Saed, F. The Role of the Agricultural Sector in the Diversification of Algerian Exports for the Period 2000-2014. M.Sc. thesis, University of Mohamed Ibn Mediaf, College of Economics, Commercial and Management Sciences, Department of Economic Sciences, 2016, pp. 19.

Khabzi, F. “The Problem of Instability in the Exchange Rate and the Role of Economic and Macro Policies in Treating It.” Journal of the New Economy, vol. 7, no. 1, 2016, pp. 147-159.

Al-Attabi, H.A. An Economic Analysis of the Role of Agricultural Exports in Agricultural Growth in Iraq for the Period 1990-2017. M.Sc. thesis, University of Baghdad, College of Agricultural Engineering Sciences, Department of Agricultural Economics, 2019, pp. 56.

Lajlaj, S.Z. “The Reality and Problems of the Foreign Trade Sector in Iraq for the Period 2003-2012.” Dinanir Journal, Iraqi University, vol. 1, no. 6, 2014, pp. 1-28.

Kozhan, R. Financial Econometrics. Bookboon Publishing ApS, 2019, pp. 74.

Dritsakis, N. “Demand for Money in Hungary: An ARDL Approach.” Academic Research Centre of Canada, 2011, Article ID 1923-7529, 1923-8401.

Al-Attabi, H.A. An Economic Analysis of the Impact of Economic Shocks on Some Agricultural Indicators in Iraq for the Period 1990-2019. Ph.D. thesis, University of Baghdad, College of Agricultural Engineering Sciences, Department of Agricultural Economics, 2022, pp. 159.