+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

This research work focuses on the nexus between of International Financial Reporting Standards (IFRS) implementation and deferred tax liabilities using a cross section of listed companies in Nigeria. The study used secondary source of data which were cross sectional from published financial statements of fifty one quoted companies in the Nigerian Stock Exchange (NSE) as at 2012 as samples. While simple percentage and mean were used to describe some of the properties of the data and provide insights about the data, paired-sample T-test and analysis of variance (ANOVA) were inferentially used to test the two formulated hypotheses. Shapiro-wilk test and Levene’s test were used to determine the normality of data and homogeneity of variances respectively. The study found out (r = 0.932; p-value <0.05) that deferred tax liabilities were significantly the same for Nigerian listed firms under IFRS and the Nigerian GAAP; on the overall, IFRS has no significant effect on the carrying amounts of deferred tax liabilities reported in the financial statements in comparison with the N-GAAP and also concluded that deferred tax liabilities were significantly the same for Nigerian listed firms under IFRS and the Nigerian GAAP; on the overall, IFRS has no significant effect on the carrying amounts of deferred tax liabilities reported in the financial statements in comparison with the N-GAAP. It is recommended that relevant Authorities should encourage Nigerian companies adopt IFRS as conversion to IFRS does not affect deferred tax liabilities.

According to Fakile et al. [1], the tax relevance of IFRS is determined by three factors, assuming no changes are made to a country's tax legislation. The first was, how closely was financial accounting related to the accounting of taxation a specific nation? The second was that, if the nation had decided to adopt the "full IFRSs" option in their entity’s annual accounts. While the third was, how much the country’s accounting standard setters consider IFRS when developing national GAAP standards and what accounting policies and principles entities can use within national GAAP. There are a number of alternative outcomes in various countries where there is some degree of association between the taxation of accounting and financial accounting, according to the belief [1].

Idowu et al. [2], however, stated that IFRSs require that all revenue and capital (including conversion costs) be confirmed by the apex tax authority in Nigeria, Federal Inland Revenue Services (FIRS) before the apex tax authority can be admitted to be qualifying capital expenditure or revenue expenditure. For the purpose of efficiency in order to overcome initial conversion problems, IFRS first-time adopters and related returns were usually given a 3 month extension for filling financial statements and related returns. The Financial Reporting Council of Nigeria (FRC) also stated that entities that have followed IFRSs in their financial statements should include their tax returns [1].

Idowu et al. [2] also stated that tax returns under IFRS for first-time adopters must comply with Section 55 of the Company Income Tax Act (CITA) 2011 and must include the statement of financial position as of the beginning of the initial comparative period when a taxpayer applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statement (i.e., a statement comparing the tax effect of IFRS adoption with GAAP), statement of reconciliation. Changes to IFRS may also affect a corporate organization’s tax liability or position, confound or streamline how an entity's financial reporting systems as well as internal control systems are run, designed and influence how top managers communicate and report with all her external stakeholders, inclusive of tax authorities, according to Oyedele.

Statement of Problem

Egbunike et al. [3] looked at tax implications on International Accounting Standards 12 adoption with reference to deposit money bank in Nigeria. It would also be of interest to know that Federal Inland Revenue Services in a circular published in March 2013 under point 5.2 that Taxpayers should submit a re-computation of Income Tax and Deferred Tax. This implies that IFRS adoption would or might impact or affect Deferred Tax Liabilities, hence the need to inquire further. This research work was the first of its type for examining the variation in the reported deferred tax liabilities across all sectors of quoted companies in Nigeria before and after the adoption of International Financial Reporting Standards. More so, the research was looking at if there was difference in Deferred Tax Liabilities among firms across the different sectors in Nigeria.

The research gap for this study was to investigate the nexus between IFRS adoption and deferred tax liabilities as over time, all previous researchers have conducted works measuring the impact or effects of IFRS on other variables such performance, quality of financial statement, position etc, for example [2,4,5], although Idowu et al. [2] examined the effects of IFRS adoption on income tax expenses all quoted entities in Nigeria, Egbunike et al. [3] also studied the tax implication of International Accounting Standards (IAS 12) adoption , evidence from Deposit Money Banks (DMBS) in Nigeria.

The broad goal of this research was to investigate the relationship between International Financial Reporting Standard (IFRS) adoption and deferred tax liabilities in Nigeria, while the specific goals were to determine whether there is a significant difference between deferred tax liabilities under IFRS and deferred tax liabilities under Nigerian GAAP and to determine whether there is a significant difference in deferred tax liabilities among firms across different sectors.

As a result, this study responds to the need of financial information users to understand the effects of IFRS adoption on deferred taxes. Changes should be expected as a result of IFRS adoption, allowing for more informed decisions. The findings of this study would have far-reaching implications for investors, management, academics, practitioners and policymakers.

Conceptual Review

Definitions: According to Nandakumar, Ghosh, Mehta and Alkafaji, IFRS is a group of standards propagated by the International Accounting Standards Board (IASB), a London-based international standard-setting body. The IASB prioritizes developing standards based on sound, clearly stated principles that require interpretation (sometimes referred to as principles-based standards). This is in contrast to sets of standards such as US GAAP, the national accounting standards of the United States, that contain significantly more application and adoption.

International Financial Reporting Standards (IFRSs) are also described by Oyedele as global Generally Accepted Accounting Principles (GAAPs) that seek to unify accounting and financial reporting globally. Inconsistencies, lack of transparency and accountability and distortion in financial reports would result from the firm's failure to apply the requirements of IFRS, resulting in poor dissemination of accounting information and financial reporting practices that are of less value to any particular group of users. Accounting standards, according to Forgarty, Hussein and Kitz, are rules that companies must follow in order to display transactions and events in their financial statements.

International Accounting Standards Committee (IASC)

The predecessor of the IASB, the International Accounting Standards Committee (IASC), was formed in 1973 through an agreement between professional accounting bodies from United states, United Kingdom, Ireland, Canada, Germany, Mexico, Japan, Holland, France and Australia, The IASC was established with the goal of developing unified accounting standards that would be accepted around the world in the public interest in order to improve financial reporting quality globally. The IASC's structure and operation have undergone several changes over the years. By the year 2000, for example, IASC's sponsorship had grown from the original 9 sponsors to 152 accounting bodies from 112 countries, i.e., all professional accounting bodies that were members of the International Federation of Accountants (IFAC).

Such fundamental changes to the IASC may have aided it in achieving its goal: Changing global standard setters' perceptions of the international nature of participation in the standard setting process.

Professional accounting bodies from around the world agreed to use their best efforts to persuade governments, standard-setting bodies, securities regulators and the business community that published financial statements should comply with IAS.

IFRS Adoption in Nigerian Context

The adoption of IFRS in Nigeria was launched in September 2010 by the Honourable Minister of Commerce and Industry, Senator Jubriel Martins-Kuye (OFR) [6]. The adoption was scheduled to begin with publicly traded companies in 2012, with all stakeholders complying by the end of 2014. This is regarded as a significant step forward for developing countries, particularly those lacking the resources to establish their own standards. The European Union adopted Regulation 1606/2002 in 2002, requiring all public entities in the region to transfigure to IFRSs beginning in 2005 [7]. Ghana, Kenya, Nigeria, Tunisia, Sierra Leone, South Africa, Zimbabwe, among other African countries involved have adopted or declared intentions to adopt the standards.

Challenges of Adopting IFRS

The following are the major challenges in implementing the IFRS Nigeria, according to Augustine [8]: Lag of accounting and auditing personnel who are technically sound and competent in teaching and adopting IFRS. Typically, the time difference and lag between the decision date to adopt and the actual implementation date is short to train and equip a good number of professional accountants and auditors capable of applying international standards competently. In Nigeria, training materials for IFRS are not sufficiently available at reasonable prices to ensure that professional personnel are well trained in large group, posing a significant challenge to IFRS acceptance. Tax considerations associated with IFRS conversion are complex, as are other aspects of a conversion. The adoption of IFRS necessitates a thorough examination of tax laws and tax administration. Accounting practices in Nigeria are governed by the Companies and Allied Matters Act (CAMA) 2020 as amended and the Statement of Accounting Standards (SAS) issued by the Nigerian Accounting Standards Board (NASB), now Financial Reporting Council of Nigeria (FRCN), as well as other existing laws such as the Nigerian Stock Exchange Act 2018 as amended, Nigerian Deposit Insurance Act 2006 as amended, Banks and Other Financial Institution Act 2020 as amended, Investment and Securities Act 2015 as amended. All of these provide some guidelines for financial statement preparation in Nigeria. The presence of these laws is not recognized by IFRS and accountants and auditors are required to follow the IFRS completely, with no overriding provisions from these laws. Nigerian legislators must make the necessary changes to ensure a smooth transition to IFRS.

IFRS and its Impact to Taxation

Although IFRS is now widely used as a reporting standard, some countries that are still in the process of implementing IFRS are unsure whether they will use IFRS financial reports or GAAP-financial reports as a basis for calculating tax income. In some other countries, tax authorities still required corporations to prepare financial reports in accordance with national GAAP for taxation purposes. The use of IFRS-financial reports for tax calculation will simplify reporting and reduce compliance costs. According to Eberhartinger et al. [9], using IFRS as a tax basis will increase ETR (Effective Tax Rates) in some industries [10].

According to Taiwo et al. [11], adopting IFRS may affect a company's tax liability’s complicate or simplify the design of a company's internal control systems and, financial reporting systems with influence how management communicates with tax authorities and other external stakeholders. Given these considerations, a successful conversion necessitates not only the commitment of the finance team but also the full participation of the tax team.

The Nigerian tax system is stated and described in the ICAN Study Pack and how the tax system affects business depends on the structure and nature of the business. Taxes are levied on businesses on an annual basis, depending on the type of business. This means that all businesses, organizations and taxable individuals are required to file a tax return to the Inland Revenue. Profits derived from corporate transactions are taxable income after they have been taxed.

Deferred Taxes

At the topmost level, IFRS 19 describes with "timing differences," also FRS 102 looks at a "timing difference plus" approach and IFRS/FRS 101 discusses "temporary differences." It is important to know that, not all temporary differences are timing differences and all timing differences are temporary. The main difference between timing differences that are also temporary differences is in the methodology or approach rather than the outcome. For instance, the method used under old GAAP to calculate deferred tax on plant and machinery (profit and loss approach) differs from the method used under IFRS (profit or loss and other comprehensive income approach) but the out-coming deferred tax asset or liability should or should not be the same in most cases. It should also be noted that under IFRS/FRS 101/FRS 102, more deferred tax balances would arise than under old GAAP, so one should expect deferred tax to arise more frequently in the future.

The following are the key points in IAS 12: Deferred tax is generally recognized as "temporary differences." "Temporary differences" are differences between the "carrying amount" of a statement of financial position asset or liability (for example, the Carry Amount (CA) of property plant and equipment) and its "tax base" (for example, the tax written-down value (TWDV) of property plant and equipment). "Temporary differences" are classified as either "taxable or deductible temporary differences." Deferred Tax Assets (DTAs) are recognized for "deductible temporary differences" and for carrying forward unused tax losses and Deferred Tax Liabilities (DTLs) are recorded for "taxable temporary differences" and future-year income taxes.

Theoretical Review

Diffusion of Innovation Theory: The significance of this theory to this study is that the accounting reform innovation has been communicated by IFRS, necessitating a comparison with the previous standards to determine the level of difference which would have arisen. Roger's theory has been described as a popular theoretical framework in technological field of implementation and diffusion. Rogers defines diffusion as "the process by which an innovation is communicated through specific channels among members of a social system over time." The theory is restricted to the exchange of information about innovation. It makes no mention of whether the innovation is positive or negative. Although it has previously been discussed that adoption of IFRS results in positive changes to financial reports, this is supported by Roger's diffusion of innovation theory for the accounting profession to keep up with the pace of development. For more than 30 years, the process of adopting new innovations has been studied and Rogers describes one of the most popular adoption models in his book, Diffusion of Innovation. Although Roger's diffusion of innovation theory is best suited to studying the adoption of technology in higher education and educational environments [12], the theory can also be applied to the accounting profession, particularly as the innovations of a global reform of financial reporting are communicated to accountants worldwide through the issuance of new sets of technical standards (IFRS) to be adopted globally. According to Ismail, the four key components of innovation diffusion are innovation, communication channels, time and social system.

New Institutional Theory (NIS)

According to Ibanichuka et al. [4], institutionalization can be viewed as a social process in which a nation accepts that local accounting standards are engrossed in the interests of international accounting harmonization. According to institutional theory, in order for organizations to sustain and survive, they must follow the rules and belief systems that exist in the environment in which they operate. Waahyunic added that when a country adopts IFRS and abandons their previous accounting standard, the main motivation should be economic, as IFRS will benefit the country economically. The economic benefit could be a reduction in the cost of capital or a significant increase in Foreign Direct Investments (FDIs) to the country's capital market. According to Touron, companies in the European Union faced strong coercive pressure to adopt IFRS in 2003, when the European Commission approved the proposal to adopt IFRS in 2005. National Accounting Standard Board, government, financial reporting council and IFRS oversight body are among the institutional factors. As a result, the study opines that the success of a nations implementing IFRS should be based on the institutional structure and factors available to operate on rather than coercive measures. As a result, structural changes should be determining factors for country IFRS convergence.

Social Comparison Theory

Idowu et al. [2] mentioned that social comparisons of oneself to others are a fundamentally psychological mechanism that influences people's behavior, experiences and judgments. The interpretation and in-dept examination of an organization's financial performance involves measuring one financial variable with another, comparing ratios with similar ratios, which could be the firm's own past ratios, industry or competitors ratios, target ratios and this is theoretically supported by social comparison theory from the field of psychology. When people are confronted with information about how others are, what others can and cannot do or what others have achieved and have failed to achieve, measuring and comparing the financial strengths and weaknesses with others and as they relate this information to themselves [2]. The importance of social comparison theory as a tool for measuring individual performance has been highlighted in the preceding discussion. The ability to gain an accurate evaluation of IFRS adoption and identify its strengths lies in the proper evaluation and comparison with a pre-existing GAAP, with specific relevance to this work. As a result, according to the theory, we would be able to reduce uncertainties in the IFRS adoption domain and learn how to improve on it.

Empirical Framework

Idowu et al. [2] used a cross-section of quoted Nigerian companies in their study on the effect of IFRS adoption on income tax expenses. As samples, secondary data were gathered from published financial reports of seventy-four publicly traded companies as of 2012. To describe the properties of the data, the simple percentage and mean were used and the paired-sample t-Test and Analysis of Variance (ANOVA) were used to test the two hypotheses. The study discovered and concluded that income tax expenses for Nigerian listed firms under IFRS and Nigerian GAAP were significantly the same; on the whole, IFRS has no significant effect on the carrying amounts of income taxes reported in financial statements when compared to N-GAAP.

Ibanichuka et al. [4] conducted an empirical study on the impact of International Financial Reporting Standard (IFRS) implementation on the financial performance of Nigerian petroleum marketing companies. Their study employed a comparative analysis to evaluate corporate performance prior to and after IFRS implemtation in the marketing sector, with a sample size of 10 quoted oil and gas marketing entities whose data were available on the Nigerian Stock Exchange (NSE) as of December 31, 2015. The study used a time series research design and the statistical tools used to test the hypotheses were one-way analysis of variance (ANOVA) and the one sample t test. Their findings revealed that neither pre-IFRS nor post-IFRS adoption has a significant effect on Return on Assets or Return on Equity; also have a significant impact on Earnings Per Share. It was concluded that there was no significant relationship between IFRS adoption and the corporate performance of Nigerian petroleum marketing entities.

Adelusi et al. [13] conducted a study to investigate the impact of IFRS adoption on the profitability of selected listed oil and gas companies in Nigeria. The focus is on these companies' liquidity, profitability and leverage when using Nigerian GAAP and IFRS. To determine whether there was a statistically significant difference in performance measurement. The work used secondary data from the financial reports of 5 publicly traded oil and gas companies. The data was analyzed using pair sample test statistics to compare the time when NG-GAAP was used and the time when companies switched to International Financial Reporting Standard. The study was conducted between 2009 and 2014. From 2009 to 2011, the companies used Nigerian Generally Accepted Accounting Principles (NG-GAAP) and from 2012 to 2014, IFRS was used to present these financial statements. The findings revealed that there was no statistically significant difference in the report of the Key Performance Indicators (KPIs) used to evaluate the company's performance.

Bassey [14] investigated the stock market reaction and the impact of IFRS adoption on the Nigerian stock market, as well as the impact of Central Bank of Nigeria (CBN) reforms on the earnings management of Nigerian banks. The outcome indicates no evidence of a significant market effect but a negative stock reaction in the medium term. Their findings highlight a mixed impact of IFRS adoption on earnings management, with a significant decrease in earnings management following CBN reforms, indicating that IFRS adoption was mistimed in Nigeria, as the fragile investor sentiment that was just recovering from the shock of the global financial crisis could have been weakened by negative market returns.

Adetula et al. [15] investigated the readiness of small and medium-sized enterprises (SMEs) in Lagos State, Nigeria, for the adoption of International Financial Reporting Standards (IFRS) and the likely challenges that might be encountered during the adoption process in their study. Their research used a descriptive survey design and data was gathered from primary sources. According to the findings, one of the main reasons why Nigeria would adopt IFRSs is because other countries have done so. Again, the results showed that the IFRS for SMEs adoption process was currently confronted with a variety of challenges that, if not addressed promptly, could prevent the effective adoption and implementation of IFRS for SMEs in Nigeria in 2014. This study suggests that the curriculum of both secondary schools and tertiary institutions be restructured to be IFRS compliant and that the cost of obtaining IFRS education be subsidized, particularly for small firms, by major accounting regulatory bodies in Nigeria.

The research design adopted for this work is the quasi-experimental design. The reason for selecting this research design is that it allows references to be made to the “before-and-after effects” of a condition on different experimental comparison group (s) under review. The total number of quoted companies was 169 as at December 2020 with 11 sectors classifications in this order: oil and gas and services, natural resources, industrial goods, information and communication technology, healthcare, financial services, conglomerates, consumer goods, construction/real estate and agriculture.

From the One-Hundred and Sixty Nine listed firms indicated above as the population of the study, 118 firms were selected using Sekeran and Boughi Sampling Table and Taro Yamane sample size determination model. However, 44 firms were dropped from the sampling frame after applying filter based on non-availability of complete data set, resulting in effective sample size of 74.

It is instructive to add that, on the ground of computational expediency such as taking the logarithm of the data to ensure normality of distribution, 51 firms were found usable for deferred tax liabilities variable. It is the considered view of this study that the further reduction in sample size did not vitiate the representativeness of the firms selected for the purpose of generalisation of findings. Secondary data were collected from the audited financial statements of the sampled firms.

The data were cross-sectionally gathered for year 2011. The choice of year 2011 was informed by data availability for the selected firms under the two reporting frameworks (i.e., the International Financial Reporting Standards and the Nigerian Generally Accepted Accounting Principles). Year 2012 was the year of transition to IFRS by listed firms in Nigeria. Companies, in the process of preparing 2012 IFRS-complaint financial statements showed comparatives for 2011 financial year. and so, from these financial statements, data on deferred tax liabilities were collected. From separately prepared N-GAAP financial statements, another set of data were gathered for the same year 2011.

With these data collection strategy, it was thus easier to fittingly compare the three variables under IFRS and N-GAAP. The data were collected from independently verifiable sources. They were also gleaned from audited financial statements. Based on these two reasons, it is the informed view of this study that there were no research-related issues relating to the validity and reliability of the study.

While simple percentage and mean were used to describe some of the properties of the data and provide insights about the data, Paired-Sample T Test, Correlation and Analysis of Variance (ANOVA) were inferentially used to test the two formulated hypotheses. Shapiro-Wilk Test and Levene Test were used to determine the normality of data and homogeneity of variances respectively.

Data Presentation, Analyses and Interpretation

Descriptive Statistics

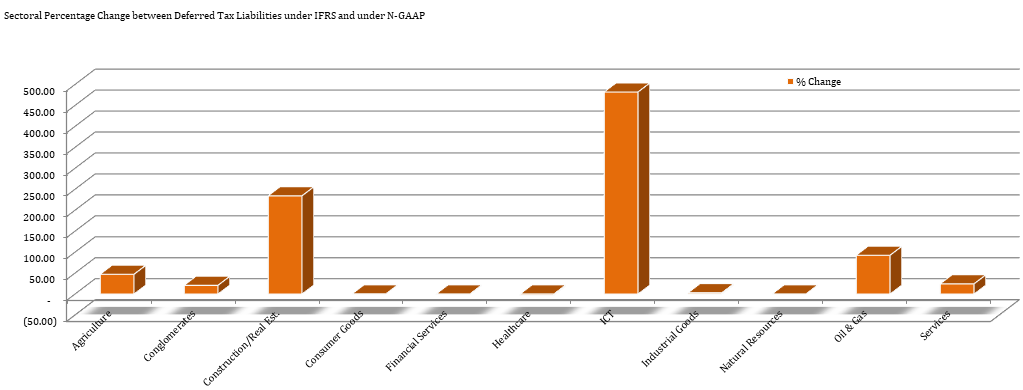

Sectoral Descriptive Statistics on Deferred Tax Liabilities: Results in Table 1 showed average sectoral percentage change between Deferred Tax Liabilities under IFRS and under the Nigerian GAAP. It could be deduced from the table that IFRS adoption necessitated the highest percentage increase of 481.8% in Deferred Tax Liabilities reported by firms in the Information and Communication Technology sector. This was followed by the Construction and Real Estate companies, whose deferred tax liabilities rose by N2.4 billion, representing 234% increase. The sector with the least percentage change was the Consumer Goods, which recorded a percentage increase of 0.21% (Figure 1).

Table 1: Sectoral Percentage Change between Deferred Tax Liabilities under IFRS and Under N-GAAP

S/No. | Sectors | DTL_IFRS (N'million) | DTL_N-GAAP (N'million) | % Change |

1 | Agriculture | 1,251.16 | 851.81 | 46.88 |

2 | Conglomerates | 283.11 | 234.76 | 20.59 |

3 | Construction/Real Est. | 3,454.78 | 1,034.07 | 234.10 |

4 | Consumer Goods | 4,395.76 | 4,386.68 | 0.21 |

5 | Financial Services | 1,384.42 | 1,397.37 | (0.93) |

6 | Healthcare | 560.99 | 578.17 | (2.97) |

7 | ICT | 83.41 | 14.34 | 481.79 |

8 | Industrial Goods | 5,544.82 | 5,383.10 | 3.00 |

9 | Natural Resources | 4.90 | 4.90 | (0.01) |

10 | Oil and Gas | 2,956.59 | 1,537.63 | 92.28 |

11 | Services | 240.83 | 193.97 | 24.16 |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation Aided by Ms-Excel, 2022), DTL_IFRS stands for Deferred Tax Liabilities under IFRS, while DTL_N-GAAP defines Deferred Tax Liabilities under Nigerian GAAP

Figure 1: Sectoral Percentage Change between Deferred Tax Liabilities under IFRS and under N-GAAP

The largest percentage increase of 481% noted for ICT companies was largely due to the 715% increase in deferred tax liabilities between N-GAAP and IFRS in respect of Chams Plc, whose deferred tax liabilities in 2011 financial year rose by N185 million, while Julius Berger contributed the most to the 234% increase for the Construction and Real Estate sector. Occasioned by IFRS, it is noteworthy that Julius Berger’s Deferred Tax Liabilities grew by a staggering N3.2 billion. However, while IFRS adoption increased the Deferred Tax Liabilities for 8 companies, only three firms had their deferred tax liabilities reduced.

Test of Independence of Data, Normality and Homogeneity of Variances

The data collected were analysed using Paired Sample T Test and Analysis of Variance, the appropriateness of the use of which depends on satisfying certain assumptions. To use Paired Sample T Test, the independence of the data collected, as well as normality are fundamental assumptions that must be satisfied. However, to use One-Way Analysis of Variance, normality assumption and homogeneity of variance assumptions must hold. These diagnostic tests were conducted and the results there from were presented below.

Independence of Data

The data were collected from different annual reports, although for the same financial year 2011. With this approach to data collection, the independence of data for one variable of interest to this study is established.

Normality

From the results in Table 2 and 3, the normality of the data for the three variables, under the IFRS reporting framework and the Nigerian Generally Accepted Accounting Principles, across the sectors is firmly demonstrated. This is because the p-values from the Shapiro-Wilk test statistics for Deferred Tax Liabilities were greater than the assumed level of significance of 5%, except for Deferred Tax Liabilities under IFRS and N-GAAP for the Services sector only. The effect of this exception is considered highly inconsequential. Therefore, the data for the variable is adjudged symmetric. Hence, they are considered suitable for the statistical techniques of Paired-Samples T-test and One-Way Analysis of Variance.

Table 2: Results from Shapiro-Wilk Test on Deferred Tax Liabilities under IFRS

Sectors | Statistic | df | Sig. |

Agriculture | 0.802 | 3 | 0.119 |

Consumer Goods | 0.911 | 12 | 0.219 |

Financial Services | 0.954 | 16 | 0.559 |

Healthcare | 0.792 | 3 | 0.095 |

ICT | 0.975 | 3 | 0.698 |

Industrial Goods | 0.958 | 3 | 0.608 |

Oil and Gas | - | 2 | - |

Services | 0.785 | 6 | 0.043 |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation Aided SPSS, 2022, ***p-value <0.01; **p-value <0.05

Table 3: Results from Shapiro-Wilk Test on Deferred Tax Liabilities under N-GAAP

Sectors | Statistic | df | Sig. |

Agriculture | 0.84 | 3 | 0.213 |

Consumer Goods | 0.953 | 12 | 0.677 |

Financial Services | 0.922 | 16 | 0.18 |

Healthcare | 0.818 | 3 | 0.159 |

ICT | 0.914 | 3 | 0.433 |

Industrial Goods | 0.956 | 3 | 0.598 |

Oil and Gas | - | 2 | - |

Services | 0.77 | 6 | 0.031 |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation Aided SPSS, 2022, ***p-value <0.01; **p-value <0.05

Homogeneity of Variances

Results in Table 4 revealed that the Levene’s statistics based on mean of 1.234 (with p-value = 0.308) is not statistically significance as their p-values were greater than the assumed 5% level of significance. This infers that the null hypotheses of homogeneity of variances for tax variable Deferred Tax Liabilities are accepted, while the alternative hypotheses are rejected. With these results, the use of One-Way Analysis of Variance is found to be fit and proper for the purpose of this research work.

Table 4: Results from Levene’s Test of Homogeneity of Variances on Deferred Tax Liabilities

Parameters | Levene Statistic | df1 | df2 | Sig. | |

Deferred Tax Liability Under IFRS | Based on Mean | 1.234 | 7 | 40 | 0.308 |

Based on Median | 1.056 | 7 | 40 | 0.409 | |

Based on Median and with adjusted df | 1.056 | 7 | 20.654 | 0.425 | |

Based on trimmed mean | 1.150 | 7 | 40 | 0.352 | |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation aided SPSS, 2022, ***p-value <0.01; **p-value <0.05

Test of Hypotheses

Hypothesis One:

H0: There is no significant difference between Deferred Tax Liabilities under IFRS and under Deferred Tax Liabilities under the Nigerian GAAP

H1: There is a significant difference between Deferred Tax Liabilities under IFRS and under the Nigerian GAAP

Results in Table 5 showed the Paired Samples Statistics on Deferred Tax Liabilities under IFRS and Nigerian GAAP, from which it can be seen that the average Deferred Tax Liabilities under IFRS for the 51 companies was 5.639384 in log 10 (equivalent to N435.9 million), while that of GAAP was 5.629843 in log 10 (equivalent to N426.4 million). Also, there is a strong, positive and statistically significant relationship between Deferred Tax Liabilities under IFRS and N-GAAP at 5% level (r = 0.932; p-value <0.05) as shown in the results in Table 6.

Table 5: Paired Samples Statistics on Deferred Tax Liabilities under IFRS and Nigerian GAAP

Parameters | Mean | N | Std. Deviation | Std. Error Mean | |

Pair 1 | Deferred Tax Liability IFRS | 5.639384 | 51 | 1.1022035 | 0.1543394 |

Deferred Tax Liability GAAP | 5.629843 | 51 | 1.0834036 | 0.1517069 | |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation aided SPSS, 2021

Table 6: Paired Samples Correlations between Deferred Tax Liabilities under IFRS and Nigerian GAAP

Parameters | N | Correlation | Sig. | |

Pair 1 | Deferred Tax Liability IFRS and Deferred Tax Liability GAAP | 51 | 0.932 | 0.000*** |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation aided SPSS, 2022, ***p-value <0.01; **p-value <0.05

Furthermore, Table 6 revealed results from Paired Samples T-Test between Deferred Tax Liabilities under IFRS and Nigerian GAAP, from which it can be inferred that there was no significant mean difference between Deferred Tax Liabilities under IFRS and under N-GAAP (t51 = 0.168, p-value >0.05), implying an acceptance of the null hypothesis that there is no significant difference between Deferred Tax Liabilities under IFRS and under Nigerian GAAP (Table 7).

Table 7: Paired Samples t-test between Deferred Tax Liabilities under IFRS and Nigerian GAAP

Parameters | Mean | Std. Deviation | Std. Error Mean | t | df | Sig. (2-tailed) | |

Pair 1 | Deferred Tax Liability IFRS- Deferred Tax Liability GAAP | 0.0095418 | 0.4044263 | 0.0566310 | 0.168 | 50 | 0.867 |

Source: IFRS and GAAP Annual Reports, 2011 and 2012, Author’s Computation aided SPSS, 2022, ***p-value <0.01; **p-value <0.05

Hypothesis Two

H0: There is no significant difference in Deferred Tax Liabilities among the firms across the different sectors

H2: There is a significant difference in Deferred Tax Liabilities among the firms across the different sectors

Table 8 contains the results from Analysis of Variance on significant difference in Deferred Tax Liabilities among firms in different sectors, from which it could well be deduced that the part of total variability (2.432) in the Deferred Tax Liabilities accounted for by the differences among the firms across the different sector is bigger than the part of the total variability in the same variable due to error (0.910). This then reflects in the F-statistics of 2.671, resulting in a p-value of 0.013, a figure less than the level of significance of 5%. Based on these results, the study is strongly persuaded to reject the null hypothesis there is no significant difference in Deferred Tax Liabilities among firms across the different sectors, while the alternative hypothesis is accepted. The inference, therefore, is that Deferred Tax Liabilities were significantly different amongst all the firms and across the different sectors (F (10, 40) = 2.671, p = 0.013).

Table 8: Results from Analysis of Variance on Significant Difference in Deferred Tax Liabilities Among the Firms Across the Different Sectors

Parameters | Sum of Squares | df | Mean Square | F | Sig. |

Between Groups | 24.323 | 10 | 2.432 | 2.671 | 0.013*** |

Within Groups | 36.420 | 40 | 0.910 | - | - |

Total | 60.743 | 50 | - | - | - |

The section presents significant findings from the analyses carried out in the preceding this section while also contextualizing these findings using the ones from related studies.

In relation to deferred tax liabilities, it was found that IFRS adoption necessitated the highest percentage increase of 481.8% in deferred tax liabilities reported by firms in the information and communication technology sector; followed by the construction and real estate companies whose deferred tax liabilities rose by N2.4 billion, representing 234% increase. The sector with the least percentage change is the consumer goods which recorded a percentage increase of 0.21%. The largest percentage increase of 481% noted for ICT companies was largely due to the 715% increase in deferred tax liabilities between N-GAAP and IFRS in respect of Chams Plc. One logical inference from the foregoing is that deferred tax liabilities, aided by the Nigerian GAAP, were grossly under-reported by firms in Information and Communication Technology sector by a staggering average of 481.8%. What this inescapably points to is that the carrying amount of non-current liabilities and by extension, total liabilities were significantly under-reported under the Nigerian Accounting Standards, particularly for Chams Plc, whose deferred tax liability was phenomenally under-reported by 715% under N-GAAP for the 2011 financial year.

For research question and hypothesis one, findings also showed that there is no significant difference between deferred tax liabilities the two reporting frameworks under review. Put differently, the inferences from the above findings are that deferred tax liabilities under IFRS and Nigerian GAAP were significantly the same; implying that IFRS adoption has no significant impact on the carrying amounts of deferred tax liabilities reported in the financial statements.

Furthermore, for research question and hypothesis two, results demonstrably revealed that Deferred Tax Liabilities were significantly not the same for the selected firms, across the different sectors of the Nigerian economy. These findings implied that deferred tax vary significantly across agriculture, conglomerates, construction and real estate, consumer goods, financial services, healthcare, ICT, industrial goods, natural resources, oil and gas and services sectors.

The findings of this work was similar to that of Idowu et al. [2] who investigated “the effect of IFRS adoption on income tax expense of quoted firms in Nigeria” whose findings revealed that IFRS adoption has no significant effect on the income tax expenses of listed companies in Nigeria. These findings are in sharp contrast with that of Egbunike et al. [3], who in their study on “Tax Implication of International Accounting Standards (IAS 12) Adoption: Evidence from Deposit Money Banks (DMBS) in Nigeria” discovered a significant variation between the reported tax figures before and after IFRSs adoption as well as income tax rates of Deposit Money Banks in Nigeria. This difference in findings might be due to the fact that the study of Egbunike et al. [3] suffers from the problem of small sample size, the use of one sub-sector of Deposit Money Banks, misspecification of methodology and fundamentally flawed research design.

The findings of this current study also differ from that of Abata [16] who in a study on “the impact of international financial reporting standards (IFRS) adoption on financial reporting practice in the Nigerian banking sector” found that quantitative differences which were statistically significant existed in the financial reports prepared under NGAAP and IAS/IFRS and thus, concluded that IFRS have impact on financial reporting in the Nigerian Banking sector. Abata [17] study had different focus that appears to be sharply different from that of the current study. This might the reason for the difference in findings. For instance, his study was not specifically delimitated on the impact of IFRS on tax reporting in Nigeria, especially in relation to the Nigerian GAAP. Abata [17] study, just like that of Egbunike and Okoye [3] also focused on one sector. The findings of this current study also contrast with that of Ishola whose study concluded that IFRS adoption has a significant effect on the financial ratios of Nigerian banks and consequently on their reporting performance. The rationales for the difference in results are similar to that of Abata [16] as well as Egbunike et al. [3].

Furthermore, the fact that the three operationalised tax variables in this current study were significantly the same under IFRS and N-GAAP implies convergence and comparability of the tax figures. This position, on the one hand, reinforces the arguments of Martin and Gatot that the advantage of using IFRS is a global comparability of financial report, while, on the other hand, disagrees that the standard change (from national GAAP to IFRS) will have impact to the tax due to the different principles used to report the corporation financial activity.

This study investigated the nexus between the International Financial Reporting Standards adoption on deferred tax reported in the financial statements of listed firms in Nigeria. Secondary data were gathered from the annual reports of 51 listed firms, after applying suitable filters on the population of 168 listed firms on the Nigerian Stock Exchange. The data collected were analysed descriptively and inferentially through the use of simple percentage, means, paired sample t-test and analysis of variance, on the bases of which the study concluded that: deferred tax liabilities under IFRS and the Nigerian GAAP were also significantly the same for Nigerian listed firms; on the overall, IFRS has no significant impact on the carrying amounts of the deferred tax reported in the financial statements in comparison with the Nigerian GAAP. The fact that the only operationalised tax variable employed in this current study were significantly the same under IFRS and N-GAAP, suggested a high degree of convergence and comparability of the tax figures under the two financial reporting framework; while there were cases of under-reporting and over-reporting of deferred taxes between the two accounting standards for some firms, these situations, on the average, were not statistically significant and deferred tax liabilities were significantly not the same for the selected firms, across the different sectors.

Recommendations

Based on the above findings of this research, this research offers the following recommendations: Federal Inland Revenue Services (FIRS) should encourage corporate tax payers to pay corporate taxes as there is no significant relationship between reported deferred tax liabilities pre and post IFRS in Nigerian. The Financial Reporting Council of Nigeria should work more in synergy with the International Accounting Standard Board to achieve greater convergence in the strictures of accounting standards for that will engender more comparable financial statements; Nigerian tax laws should be reviewed at regular intervals to ensure more currency in order to make Nigerian firms internationally competitive. The Financial Reporting Council of Nigeria should also seek further ways of collaborating with tax authorities such as the Federal Inland Revenue Service, States Internal Revenue Service, Joint Tax Board in order to entrench practices that discourage tax evasion, avoidance, aggressive tax planning and tax inversion.

Fakile, A.S. et al. “The Impact of International Financial Reporting Standards on Taxation.” International Journal of Business and Social Science, vol. 4, no. 10, August 2013.

Idowu, K.A. et al. “Effects of IFRS Adoption on Income Tax Expenses of Quoted Companies in Nigeria.” Journal of Accounting and Finance Management, vol. 7, no. 4, 2021, pp. 24-46.

Egbunike, P.A. et al. “Tax Implications of International Accounting Standards (IAS 12) Adoption.” International Journal of Social and Administrative Sciences, vol. 2, no. 2, 2017, pp. 52-62.

Ibanichuka, E.A. et al. “International Financial Reporting Standards Adoption and Financial Performance of Petroleum Marketing Entities in Nigeria.” International Journal of Advanced Academic Research, vol. 4, no. 2, February 2018, pp. 1-15.

Demaki, D.O. “Prospects and Challenges of International Financial Reporting Standards to Economic Development in Nigeria.” Global Journal of Management and Business Research, vol. 13, no. 1, 2013, pp. 69-73.

Madugba, J.U. et al. “Corporate Tax and Revenue Generation: Evidence from Nigeria.” Journal of Emerging Trends in Economics and Management Science, vol. 6, no. 5, 2015, pp. 333-339.

Iyoha, F.O. et al. “Adopting International Financial Reporting Standards (IFRS): A Focus on Nigeria.” International Journal of Research in Commerce and Management, vol. 1, no. 2, 2011, pp. 35-40.

Augustine, A. “A Proposed Rule-Roadmap for the Adoption of International Financial Reporting Standards (IFRS) in Nigeria.” American Journal of Economics, Special Issue, June 2012, pp. 41-45.

Eberhartinger, E. et al. “What If IFRS Were a Tax Base? New Empirical Evidence from an Austrian Perspective.” Accounting in Europe, 2007, pp. 141-168.

Haverals, J. “IAS/IFRS in Belgium: Quantitative Analysis on the Impact on the Tax Burden of Companies.” Journal of International Accounting, Auditing and Taxation, 2007, pp. 69-89.

Taiwo, F.H. et al. “Empirical Analysis of the Effect of IFRS Adoption on Accounting Practices in Nigeria.” Archives of Business Research, vol. 2, no. 2, April 2014, pp. 1-14.

Brennan, K. “A Stakeholder Analysis of the BP Oil Spill and the Compensation Mechanisms Used to Minimize Damage.” Journal of Management Studies, vol. 39, no. 1, 1995, pp. 1-21.

Adelusi, A.I. et al. “The International Financial Reporting Standard (IFRS) Adoption and the Profitability of Selected Quoted Oil and Gas Companies in Nigeria.” International Journal of Operational Research in Management, Social Sciences and Education, vol. 3, no. 2, September 2017.

Bassey, O.U. ICAN Practice and Revision Kit (Skills and Professional Levels): Taxation and Advanced Taxation. Best Brain Bookshops, 2016.

Adetula, D.T. et al. “International Financial Reporting Standards (IFRS) for SMEs Adoption Process in Nigeria.” European Journal of Accounting, Auditing and Finance Research, vol. 2, no. 4, June 2014, pp. 33-38.

Abata, A.M. “Impact of IFRS on Financial Reporting Practices in Nigeria (A Case of KPMG).” Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics, vol. 1, no. 1, 2015.

Abata, M.A. “The Impact of International Financial Reporting Standards (IFRS) Adoption on Financial Reporting Practice in the Nigerian Banking Sector.” Journal of Policy and Development Studies, vol. 9, no. 2, February 2015.