+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

The study examined the influence of Internal Auditor attributes on fraud prevention in the Ministries, Departments and Agencies (MDAs) in Akwa Ibom State. The study was prompted by persistent fraudulent practices in the Nigerian public sector space. Survey research design was adopted using questionnaire to gather data from 107 internal auditors sampled for the study. Descriptive and inferential statistics were applied in the data analysis. The result of the analysis showed that internal auditors effectiveness, independence, training, experience and qualification influenced fraud prevention. The R2 value of 95.2%, adjusted R2 of 95% and F-cal of 406.80 showed the results were statistically significant and suitable for policy alignment that the independent variables are good influencers of fraud prevention in the public sector. It was recommended that conducive environment be created for internal auditors to function as well as regular review of policies relating to fraud prevention by policy makers.

Various surveys and researches have been carried out in different countries with the aim to ascertaining the true scale and costs of fraud to businesses and societies. On the whole, findings varied significantly from different researchers which made it difficult to ascertain the exact implication of fraud on organizations. However, a great number of the surveys established the prevalence of frauds within organizations especially in government ministries and remained serious and costly problem to virtually every unit of organizations particularly in developing economies of the world.

Despite the serious risks fraud poses to business and countries, many organizations and government still seem not to have efficient formal systems and procedures in place to prevent, detect and respond to this menance. Even when they exist, the implementation and application seem inefficiently applied. Owing to increasing unethical practices, deceitful activities and the frequently recurring financial impropriety, it is now more demanding and of necessity the services of internal audit function in both public and private organizations [1]. The main objective of internal auditing has been assumed to ensuring financial effectiveness and efficiency of operations, promotion of accountability and deterrence to any fraudulent activities, safeguard assets of the organizations and minimize losses that may occur due to dereliction of duty.

Internal audit units of organization are supposed to be manned by competent personnel named “Internal Auditors” with special attributes that made them stand out in the organization as watchdogs, policeman, whistle-blowers and the likes. How the internal auditors have applied their privileged position to minimize the recurrences of fraud in the Nigeria Public Sector organizations given their differentia requires empirical investigations. Hence, this research aims at ascertaining how internal auditors attributes has contributed to fraud prevention in government Ministries, Departments and Agencies (MDAs) in Akwa Ibom State, Nigeria.

Objectives of the Study

The objective of the study is to evaluate the composite influence of internal auditors’ attributes (effectiveness, independence, training, experience and qualifications) on fraud prevention in MDAs of government in Akwa Ibom State, Nigeria.

Research Questions and Hypothesis of the Study

The research question raised for this study is stated as: What is the composite influence of internal auditors attributes on fraud prevention in selected MDAs of government in Akwa Ibom State, Nigeria?

In line with the research objective and question, the hypothesis of the study is developed and stated in null form as follow:

Ho: Internal auditors attribute do not significantly affect fraud prevention in selected MDAs of government in Akwa Ibom State, Nigeria

Significance of the Study

The results of this empirical investigation is significantly relevant in the light of the recent search by stakeholders for procedures that could protect, improve and create efficient and effective use of public fund and ensuring financial management assurance in government. The findings would benefit government ministries, departments and agencies in policy formulation and implementation in respect to internal control issues, researchers, consultants as well as an addition to existing empirical literature in this area of interest.

The remaining part of this paper cover review of related literature, methodology of the study, results and findings and summary and conclusion.

Review of Related Literature

The conceptual issues, theoretical review, empirical review and gap in the literature are discussed in this section.

Conceptual Framework

The following concepts are discussed-Public sector, internal auditing and attributes of internal auditor.

Public Sector

The public sector comprises of all government organizations, institutions, agencies and other entities that are funded through public resources such as taxes, fines and so on to render public services, program and deliver goods and services to the general public [2].

In other words, public sector is all organizations which are not privately owned and operated but which are established, ran and financed by government on behalf of the public. These entities include all government ministries, departments and agencies. In Akwa Ibom State, there are twenty ministries and one hundred and twenty seven departments and agencies [3].

In the Nigerian public Sector entities, the issues of weak institutions, inefficiency and ineffectiveness in processes and procedures in the conduct of government business have been recurring reports in the broadcast media; thereby begging for answers the workability of the internal control systems which are manned by internal auditors with their lofty qualities despite varying degrees of reorganization and realignment of programs which should engendered improved performance and more reliable services by public agencies.

Internal Auditing and Attributes of Internal Auditors

The Statement on Auditing practice (SAP-6) of the institute of Chartered Accountant of India describes internal audits as “the plan of organization and all the methods and procedures adopted by the management of an entity to assist in achieving management’s objective of insuring, as far as possible, the orderly and efficient conduct of its business, including adherence to management policies, the safeguarding of assets, prevention and detection of fraud and error, the accuracy and completeness of accounting records and timely preparation of reliable financial information. On the other hand, internal audit is a critical appraisal of functioning of various operations of an enterprise including the functioning of internal check system. Accuracy, completeness, reliability and timeliness of accounting information are tested and reported for remedial in cases of slack. Internal audit unit in an organization is described as a unit saddled with the responsibility of giving objective assurances about the operation of the organization with the aim to boosting the effectiveness of the operation of the establishment. It is an independent action geared towards helping an organization achieve its mandate through a systemic effort to improve risk management effectiveness and control processes. How well this is achieved is a function of the attributes of the internal auditor. Ali et al. [4] argued that, in public sector institutions, the functions of Internal Audit embrace possibilities for stimulating responsibility and improve government performances.

Rafay and Shakeel [5] opined that the accelerated evolution of internal auditing functions is anchored on its effectiveness, training, staffing and qualification, independence, experience and the ability to plan, control and record their work. These combined attributes should aimed at ensuring more efficient operations, accountability, sufficient, knowledge and experience to handle problematic circumstances which could arise from fraudulent situations.

Fraud and Fraud Prevention

Bierstaker et al. [6] defined fraud as “all multifarious means which human ingenuity can devise and which are resorted to by one individual to get advantages over another by false suggestions or suppressions of the truth. It includes all surprises, tricks, cunning or dissembling and any unfair way by which another is cheated. The term fraud is also commonly used to describe a wide variety of dishonest behaviours such as deception, bribery, corruption, forgery, false representation, collusion and concealment of material fact.

In the public sector, a suitable summary of fraud within the context of the study is an act of obtaining financial value by trick or deceit through inflation of contract, kickbacks, paying or collecting money for non-existing commodity, misappropriation of cash, manipulation of accounts to disclose false position, wage fraud, computer frauds and ghost workers, embezzlement as well as misallocation of budgeted funds. Although, the responsibilities for fraud prevention and detection rest with the Board of Directors [7], the audit committee, legal counsel and internal auditors, a clinical analysis would reveal that the internal auditors are the feeder unit of information for the other parties to functions and to fulfil their mandate. Consequently, the need to harness the attributes of internal auditors in fraud prevention in the public sector.

Theoretical Framework

Two theories, the theory of inspired confidence and the institutional theory formed the theoretical foundations of the study.

The Theory of Inspired Confidence

This theory was advanced in the late 1920s by the Dutch Professor Limperg with the hope to address both the demand and the supply of audit services. Limperg in 1920 argued that auditing of management activities is necessary to inspire confidence in the stakeholders who may not trust management entirely to be fair in their report since the management are expected to prepare reports that meet divergent interest of different stakeholders. The idea here is that auditors are expected to audit the information provided by the management to check for biases and deviation from normalcy. This theory is relevant to this research work because the public sector is accountable to the public for funds used which are gotten from funding sources such as taxes, grants and other sources.

The Institutional Theory

Institutional theory seeks to explain the processes and reasons for organizational behavior as well as the effect of organizational behaviour patterns within a broader, inter-organizational context. The foundations of institutional theory as it is currently understood took root between 1977 and 1983 amid a broader search for understanding the elements that support successful and sustained organizational performance. The theory is adopted in this study because it identified the role of internal auditors has being significant in improving corporate governance mechanism of public sector organization as a way of streamlining processes and controlling of operations for effectiveness.

Review of Related Empirical Literature

Some of the related empirical researches reviewed for the study are presented in a summarized form on Table 1.

Gap in the Literature

The review of empirical literature indicated that different studies had been conducted on the determinant of effectiveness of internal audit but none of the reviewed studies looked at attributes of internal auditors and fraud prevention in the public sector, which this study focused on.

The survey research design was used in the study to gather data from one hundred and seven internal auditors determined using Taro Yamene’s statistical formular. The respondents sampled were heads of Internal audit units in the Akwa Ibom State Ministries, Departments and Agencies (MDAs).

Sources of Data and Instrument of Data Collection

The data used for this study was primary in nature obtained through structured questionnaire designed using five-point Likert-Scale with appropriate sections for the independent variables. To ensure the validity of the instrument, three copies of the instrument were discussed with other accounting lecturers for inputs and amendments. The reliability of the instrument used was carried out by computing the Cronbach’s Alpha Coefficient for each variable using the questions in the instrument. The results are shown in Table 2.

The Cronbach’s Alpha Coefficients were all above 70% index and hence; the instrument adjudged suitable for use in the study.

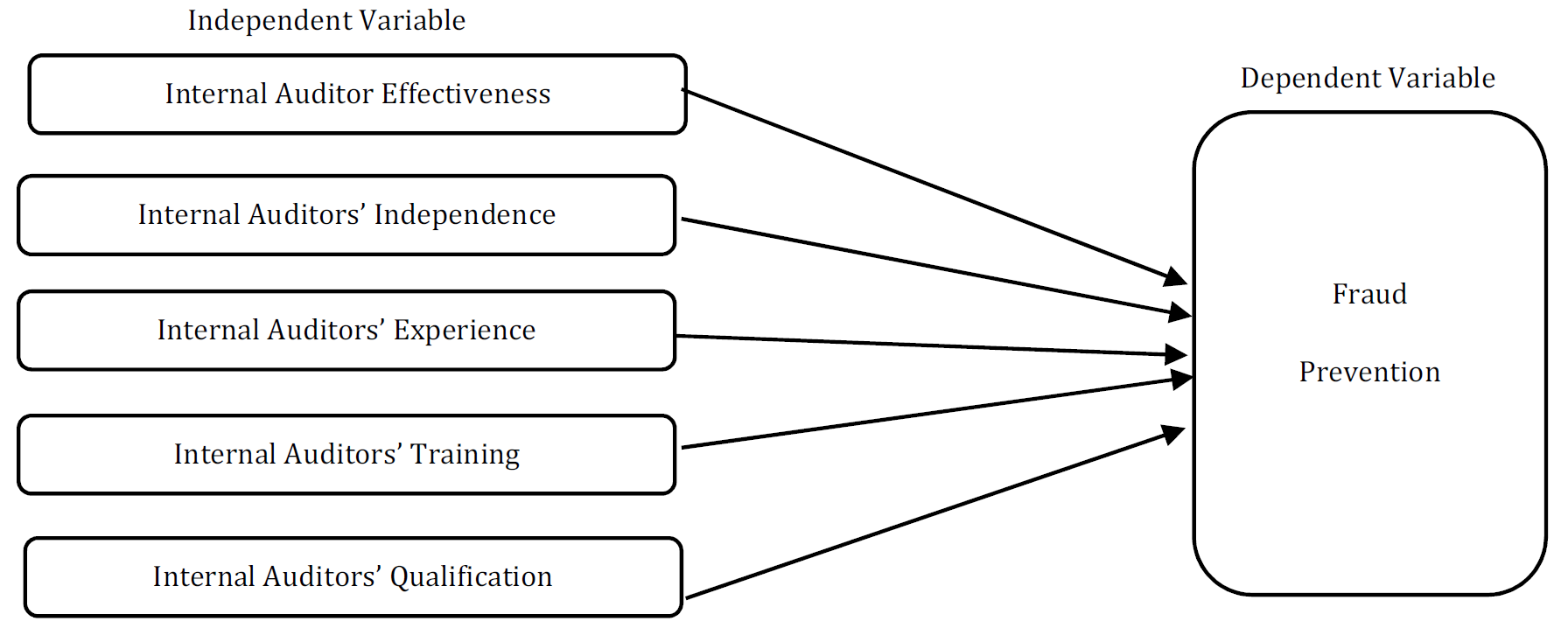

Theoretical Specification of Model

The theoretical model specified for this study is in line with the research interest as shown in Figure 1.

Empirical Specification of Model

The empirical model for this study is expressed in the following econometric model which is developed to test the relationship between the dependent and independent variables.

FP = ƒ (IAEFF, JAINDEP, JATRA, IAQUA, JAEXP)

(1)

Table 2.1 Summary of Empirical Literature

S/N | AUTHOR(S) | TOPIC | METHODOLOGY | FINDING(S) |

1. | Drogalas, Karagiogos and Arampatzis (2015) | Factors associated with internal audit effectiveness: Evidence from Greece | Data were collected by means of mailed survey and analysed using factor analysis and regression analysis | Results indicated that the main factor affecting internal audit effectiveness were quality of internal audit, competence and independence of internal audit term and management support |

ii. | Chambers and Odar (2015) | Factors affecting the internal audit effectivness in Tunisian Organization | Survey research design was adopted involving use of questionnaire to gather data from 148 chief audit executives of Tunisian organizations. | Result revealed that the effectiveness of internal auditing was influenced by the independence and the objectivity of internal auditors, management support for internal audit the use of internal audit function as a management training ground and the sector of organization |

iii. | Tarekegn (2015) | Determinants of internal auditor’s effectiveness: case of Ethiopian Public Sector | Primary data were collected from managers and internal auditors of 30 public sector organizations Likert-scale type questionnaire was used to collect data, which were analysed using the Ordinary Least Square (OLS) linear regression model. | The findings of the study revealed that organizational independence of internal auditors was the most dominant determinant of internal auditors’ effectiveness with positive significant effect. The presence of internal audit charter in public sector also had Positive effect on internal auditors’ effectiveness. |

iv. | Hella and Mohammed (2016) | Factors affecting the internal Audit effectiveness in Tusisian organization | Survey research design involving the use of questionnaire to elicit responses from chief audit executives of one hundred and forty eight (148) Tunisian Organizations. Multiple regression analysis and factor analysis were used to analysed data. | The findings revealed that the effectiveness of internal audit function was influenced by the management support for internal audit. It linked management support to hiring trained and experienced staff, providing sufficient resources, enhancing the relationship with external auditors and having an independent internal audit department. |

v. | George, Edward and Sampson (2016) | Determinants of internal audit effectiveness in decentralized local government administrative systems | Data was gathered using survey research design with questionnaire. Multiple regression analysis was used to examine the association between determinant of audit effectiveness of internal audit function. | The study revealed that there existed high quality of audit work due to compliance with the international standards on auditing and local audit legislations. Professional proficiency organizational independence and career advancement were found to have statistically significant positive relationship with internal audit effectiveness |

vi. | Julius and Patrick (2016) | Determinants of internal audit effectiveness of public sector: a case study of Rwanda revenue authority | Descriptive research design was employed for the study involving questionnaire administered to 89 employees of Rwanda Revenue Authority | The results indicated that management support was the most significant in explaining the effectiveness of internal audit that with management support every other variables would be effective. |

Vii | Fetus (2016) | Determinant of internal audit effectiveness in road construction sector: Case Study in Ethiopian Road Authority | Use of structured questionnaire to gather data from internal audit staff of Ethiopian Roads Authority and analysed using descriptive Statistics. | The finding revealed that all of the five independent variables made 58.7% of the Construction for internal audit effectiveness in Ethiopian Road Authority. |

viii. | George, Pazarskislo and Angelic (2017) | The effect of internal auditor responsibility and training in fraud detection | Survey research design using primary data obtained through questionnaire to gather data from 60 respondents. Data were analyzed using descriptive statistics. | Their analysis shared that audit effectiveness responsibility and auditor responsibility and auditor training affected positively and significantly the detection of fraud. |

ix. | Salma, Ibrahim and Almula (2018) | Determinants of Internal audit effectiveness audit effectiveness: Case study of Sudan Public Sectors | The data were collected through a likert-scale type questionnaire on a sample of 41 internal auditors and 27 managers. Descriptive and correlation analysis and multivariate regression model were used to analysis. the data | The results showed that there was a significant positive relationship among the factors analyzed. |

x. | Ayitenew and Lakech (2018) | Determinants of internal audit effectiveness: evidence from Gurage Zone | The researchers used descriptive and explanatory research design for the study 60 respondents were the sampled size who were administered the research instrument | The result of the study indicated that quality of internal audit, independency of internal audit and proficiency of internal auditors positively affect internal audit effectiveness. |

xi. | Alqudah, Amran and Hassan (2019) | Determinants of internal auditors’ effectiveness in public sector | Data were collected through questionnaire from 117 financial managers and internal audit (AI) managers of the Jordanian public sector institutions. The collected data were analyzed using Partial Least Squares Structural Equation Modeling (PLS-SEM) | The result revealed that top management empowerment, and internal auditors independence are the factors which positively and significantly affect the internal auditors’ effectiveness. |

xii. | Alemzewed (2019) | Determinants of Internal audit effectiveness in Ethopia: A case Study of selected budgetary public sector entities | The researcher used mixed research method by employing quanlitative and quantitative research method. 85 copies of questionnaire constructed in 5 point Likert scale were used. Data were analysed using regression analysis. | The finding revealed that internal audit quality and management supports were statistically significant with the effectiveness of internal unit. Independence of internal audit and competence of internal audit team were statistically insignificant with the effectiveness of internal audit. |

xiii. | Armstrong and Yidana (2019) | Determinants of internal audit effectiveness in selected hospital within Kumasi Metropolis | Survey research design was used to gather data which were analyzed with descriptive statistics | The study revealed that all the determinants of internal Audit effectiveness such as organizational independence, effective internal controls adequate internal audit charter, frequent internal audit meeting and were statistically significant competent internal audit staff. |

xiv. | Ngugi (2020) | Determinant of Internal audit and its effectiveness in public sector in Kenya. A case of the national treasury | A sample of 139 internal auditors were selected from a target population of 395 internal auditors drawn from the National Treasury in Kenya using stratified random sampling technique. Data were collected through online questionnaire sent through emails. Descriptive and regression analysis were used to analyze the data | The findings from the analyzes showed that the four independent variables had positive and significant effect on internal audit effectiveness such as top management support, management information system organizational independence and training |

xv. | Mvelo, Ayogeboh, Lulu and Oludayo (2021) | Determinants of Internal audit effectiveness in a public higher education institution | Survey research design involving use of questionnaire to collect data was employed by the researchers. Data collected were analyzed using multiple regression analysis to examine the association between the effectiveness of internal audit function and six principal factors | Result from the principal component analysis (PCA) revealed the determinant enhanced effective internal audit and performance in a public higher education institution. |

Source: Researchers’ Compilation (2022)

Figure 1: Theoretical Model

Source: Researchers’ Conceptualization (2022)

Table 2: Crombach Alpha Coefficients

Variable | Cronbach’s Alpha | No of Items |

Fraud prevention | 0.873 | 8 |

Effectiveness | 0.781 | 5 |

Training | 0.782 | 5 |

Qualification | 0.766 | 5 |

Independence | 0.815 | 7 |

Experience | 0.786 | 5 |

Source: Researcher’s Computation (2022)

Table 3: Measurement of Variable and Apriori Expectations

Variables | Type | Measurement | Apriori expectations |

Fraud Prevention | Dependent | Sum of questionnaire Items responses | - |

Internal Auditors’ Effectiveness | Independent | Sum of questionnaire Items responses | Positive |

Internal Auditors’ Independence | Independent | Sum of questionnaire Items responses | Positive |

Internal Auditors’ Training | Independent | Sum of questionnaire Items responses | Positive |

Internal Auditors’ Experience | Independent | Sum of questionnaire Items responses | Positive |

Internal Auditors’ Qualifications | Independent | Sum of questionnaire Items responses | Positive |

Source: Researchers’ Compilation (2022)

Specifically:

FP = β0+β1IAEFF+β2 IAINDEP+β3IATRE+β4IAQUA+β5IAEXP+ƹ

(2)

Where:

FP = Y is the independent variable (Fraud Prevention)

P = Regression Constant or Intercept

β1+β5 = Internal Auditors’ Effectiveness

IAINDEP = Internal Auditors’ Independence

IATRA = Internal Auditors’ Training

IAQUA = Internal Auditors’ Qualifications

IAEXP = Internal Auditors’ Experience

![]() = Stochastic Error Term

= Stochastic Error Term

Measurement of Variable and Apriori Expectations

The Variable of the Study are measured with their apriori expectations as shown on Table 3.

Method of Data Analysis

Multiple Linear regression analysis technique and descriptive statistics are employed in the analysis of data. The decision rule for acceptance or rejection of the hypothesis is based on 5% level of significance for calculated F and p-values. The R, R2 adjusted R2 and Durbin-Watson (D-W) statistic are also used in analysis of the data. The descriptive statistic acceptance range is 2.5 average value and above.

The results of data analyses are disclosed in this section with the discussion of the findings.

Descriptive Analysis of Data

The descriptive analysis of the responses to the questionnaire on each variable of interests studied is presented in this section of the paper.

Descriptive Analysis on Fraud Prevention Activities

The responses relating to fraud prevention indices are presented on Table 4.

From the Table 4 which shows descriptive statistic values (means values) for indices of fraud prevention in the MDAs in Akawa Ibom State. All the indices met the average value of 2.5 mean point and above except for the management regularly reviewing entity’s policies in the light of changing environment and economic conditions with mean value of 2.40. This implies there is a lag between current operational realities and what should ordinarily be done by those saddled with management of entities for fraud prevention.

Table 4: Descriptive Analysis of Responses to Fraud Prevention Activities

Weight Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

Standard procedures are put in place for all financial transactions | 15 (0) | 0 (0) | 19 (38) | 57 (171) | 16 (64) | 107 (273) 2.55 |

The organization ensures approval is given by appropriate authority(ies) before financial transactions are effected | 8 (0) | 7 (7) | 0 (0) | 62 (186) | 30 (120) | 107 (313) 2.93 |

Internal controls are closely monitored for possible violations that may result in suspicious transaction occurring | 14 (0) | 6 (6) | 0 (0) | 67 (201) | 20 (80) | 107 2.68 (287) |

Internal control system layers are instituted and must be followed for transaction approval | 7 (0) | 21 (21) | 0 (0) | 67 (201) | 12 (48) | 107 2.52 (270) |

Management regularly assess risk exposures of the entity | 6 (0) | 4 (4) | 0 (0) | 37 (111) | 60 (240) | 107 3.32 (355) |

Internal audit unit regularly check companies with laid down policy and procedure. | 0 (0) | 0 (0) | 0 (0) | 31 (93) | 76 (306) | 107 3.71 (397) |

Management regularly review entity’s policies in the light of changing environment and economic conditions. | 6 (0) | 30 (30) | 0 (0) | 57 (171) | 14 (56) | 107 2.40 (257) |

All staff/employees are often subjected to background checks | 8 (0) | 0 (0) | 0 (0) | 44 (132) | 55 (220) | 108 3.29 (352) |

Source: Researchers’ Computation (2022), U = Undecided, SD = Strongly Disagree, D = Disagree, A = Agree and SA = Strongly Agreed

Table 5: Responses on Internal Auditor’s Effectiveness

Weight Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

Existence of Internal audit department in the organization increases corporate control of errors irregularities and fraud | 6 (0) | 35 (35) | 0 (0) | 27 (81) | 39 (156) | 107 2.54 (272) |

Internal audit unit in the organization usually furnish authorities with both financial and non-financial information required to safeguard the system against fraud | 0 (0) | 48 (48) | 0 (0) | 19 (57) | 40 (160) | 107 2.50 (265) |

There are well defined disciplinary consequences to perpetrators of fraud in the organization

| 6 (0) | 0 (0) | 0 (0) | 66 (198) | 35 (140) | 107 3.16 (338) |

Management of the organization creates a positive control working environment in order to discourage rationalizing behavior to cement fraud | 29 (0) | 42 (42) | 0 (0) | 24 (72) | 12 (48) | 107 1.51 (162) |

The organizations code of conduct supports the organization’s internal control systems | 5 (0) | 2 (2) | 0 (0) | 75 (225) | 25 100) | 107 3.06 (327) |

Source: Researchers’ Computation (2022)

Table 6: Responses to Internal Auditors’ Training

Weight Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

Internal audit staff are provided with regular audit training courses that are specifically about the prevention of fraudulent activities | 21 (0) | 0 (0) | 27 (54) | 41 (123) | 18 (72) | 107 2.33 (219) |

The management exposes/introduces internal audit staff to new/current technologies that help to prevent fraud | 15 (0) | 0 (0) | 44 (88) | 42 (126) | 6 (24) | 107 2.22 (238) |

Internal auditors are provided with training opportunities in specific operations/specially in a bid to enhance skill towards fraud prevention | 9 (0) | 30 (30) | 5 (10) | 47 (141) | 16 (64) | 107 2.28 (245) |

Source: Researcher’s Computation (2022)

Descriptive Analysis of Internal Auditors’ Effectiveness

The descriptive analysis of internal auditors’ effectiveness is presented on Table 5.

From Table 5, involving responses to internal Auditors’ effectiveness, all the indices met the acceptance or tolerance level except for the index “management of the organization creates a positive control working environment in order to discourage rationalizing behavior to commit fraud” This implies that available controls do not take cognizance of creating controls that discourage fraudulent behaviours.

Descriptive Analysis of Internal Auditors’ Training

The descriptive analysis of internal auditors’ training is presented on Table 6.

Table 6 revealed that the mean scores of responses to internal auditors’ training questions had mean values within the range 2.00 and 2.33. This implies that all the indices relating to training fell short of the acceptance range. It reveals that training of internal auditors is not accorded priority, hence not taking seriously dispute it importance in fraud prevention.

Table 7: Responses to internal Auditors’ Qualification

Weight/Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

Internal Auditors in the Organization are Certified Auditor

| 8 (0) | 0 (0) | 59 (18) | 31 (93) | 9 (36) | 107 2.31 (247) |

The qualification of internal Auditor in the organization enhances the quality of internal audit exercises | 6 (0)

| 0 (0) | 0 (0) | 75 (225) | 26 (104) | 107 3.08 329 |

The qualification of internal auditors helps to identify any non-compliant activities

| 2 (0) | 0 (0) | 4 (8) | 59 (177) | 42 (168) | 107 3.30 (353) |

The qualification of internal Auditors helps them to performed well in discharging the duties

| 5 (0) | 0 (0) | 61 (122) | 32 (96) | 9 (36) | 107 2.40 (254) |

Qualified internal Auditors perform internal audit services in accordance with international Auditing Standards | 15 (0) | 0 (0) | 54 (162) | 18 (54) | 20 (80) | 107 2.77 (296) |

Source: Researchers’ Computation (2022)

Table 8: Responses to Internal Auditors Independence

Weight/Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

The Internal Auditor performs auditing activities without any interferences from anybody

| 14 (0) | 0 (0) | 27 (54) | 58 (174) | 8 (32) | 107 2.43 (260) |

Internal Auditor feels free to include any audit findings in their report

| 20 (0) | 2 (2) | 0 (0) | 83 (249) | 2 (8) | 107 2.42 (259) |

Internal auditors are immune from any internal pressure in conducting their work

| 16 (0) | 0 (0) | 47 (94) | 32 (96) | 12 (48) | 107 2.22 (238) |

Internal Auditor has free and unrestricted access to all operations, assets and transaction records and personnel in obtaining evidence | 6 (0) | 0 (0) | 37 (74) | 23 (69) | 41 (164) | 107 2.87 (307) |

Source: Researchers’ Computation (2022)

Table 9: Responses to Internal Auditors’ Experience

Weight Scale/Total Weighted Responses | U 0 | SD 1 | D 2 | A 3 | SA 4 | Average |

Internal Auditors’ experience affect the nature of Internal Control system | 12 (0)

| 0 (0) | 36 (72) | 42 (126) | 17 (68) | 107 2.50 (266) |

The internal auditors experience easily determine the nature and frequency of non-compliance activities | 4 (0) | 0 (0) | 46 (92) | 36 (108) | 21 (84) | 107 2.65 (284) |

Internal Auditors have the experience and expertise to address fraud risks problems within the organization

| 10 (0) | 0 (0) | 0 (0) | 57 (171) | 40 (160) | 107 3.09 331 |

The nature of reports, recommendations, criticisms and information provided by internal Auditors assists fraud minimization | 6 (0) | 0 (0) | 38 (76) | 25 (75) | 38 (152) | 107 2.83 303 |

Source: Researchers’ Computation (2022)

Descriptive Analysis of Internal Auditors’ Qualification

The responses relating the internal auditors’ qualification variable indices are presented on Table 7.

Table 7 revealed the mean scores of responses to internal auditors’ qualification questions. The mean scores revealed that internal auditors’ certification had 2.31 mean score and qualification of internal auditors as tool to performance of duties 2.40 mean score. This implies that not all internal auditors are certified professionally does impacting discharge of their duties. Other indices considered on the internal auditors’ qualification met the 2.5 mean score affirming the relevance of Internal Auditors Qualification in Fraud prevention.

Descriptive Analysis of Internal Auditors’ Independence

The responses on Internal auditors’ independence indices are presented on Table 8.

From Table 8, the statistics revealed that all the indices of internal auditors independence failed the mean score threshold of 2.5, except for unrestricted access to records and books of account. The implication is that internal Auditors’ in government organizations are relatively not independent in the discharge of their duties.

Descriptive Analysis of Responses on Internal Auditors’ Experience

The responses in respect of internal auditors’ experience variable indices are presented on Table 9.

The Table 4.6, all the indices relating to Internal auditors’ experience met the acceptance threshold of 2.5 means score and above, thus affirming the necessity of experience in fraud prevented in MDAs in Akwa Ibom State.

Inferential Statistical Analysis of Hypothesis of the Study

The test of hypothesis for this study is conducted using the multiple regression results shown on the model summary, ANOVA and coefficients of the regression output as shown on Table 10-12.

The null hypothesis was stated as “internal auditors” attributes and experience do not significantly affect fraud prevention in selected MDAs in Akwa Ibom State, Nigeria”. From the regression output (ANOVA), based on the decision rule, the null hypothesis of the study is rejected since the p-value 0.00 is less than 0.05 and the calculated F-value of 406.798 is greater than the critical F-value of 1.983.

This implies, when the independent variables are jointly regressed, they are potent to fraud prevention in government establishments.

Table 10: Model Summary for Hypothesis Testing

Model | R | R Square | Adjusted R2 | Std. Error of the Estimate | Dubin Watson |

1 | 0.976a | 0.952 | 0.950 | 0.66339 | 0.866 |

aPredictors: (Constant), IAEFF, IAINDEP, IATRA, IAQUAL, IAEXP, bDependent Vairable: FP

Table 11: ANOVA

Model | Sum of squares | Df | Mean square | F | Sig. |

1. Regression | 895.127 | 5 | 179.025 | 406.798 | 0.0006 |

Residual | 44.889 | 102 | 0.440 | - | - |

Total | 940.016b | 107 | - | - | - |

aPredictors: (Constant), bDependent Vairable: FP

Table 12: Regression Coefficients

| Model 1 | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collineraity | ||

B | Std. Error | Beta | Tolerance | VIF | |||

Constant | 4.945 | 1.620 |

| 3.052 | 0.003 | - | - |

IAEFF | 0.651 | 0.114 | 0.578 | 5.687 | 0.000 | 0.240 | 4.171 |

IATRA | 0.053 | 0.066 | 0.041 | 0.798 | 0.427 | 0.328 | 3.048 |

IAQUAL | 0.173 | 0.105 | 0.142 | 1.655 | 0.101 | 0.198 | 5.053 |

IAINDEP | 0.006 | 0.098 | 0.005 | 0.059 | 0.953 | 0.208 | 4.806 |

IAEXP | 0.259 | 0.086 | 0.227 | 3.014 | 0.003 | - | - |

Source: Researchers’ Computation (2022), aDependent variable: FP

From the findings, 95.2% fraud prevention activities are attributed to the independent variable studied and that there exists 97.6% correlation between fraud prevention and Internal Auditors’ attributes.

Evaluating the independent variables on an item by item basis, all the indices relating to internal auditors’ effectiveness, shows each item was potent in fraud prevention. The t-value was 5.687 and p-value 0.0000 which are statistically significant, indicating that internal auditors’ effectiveness is a good attribute in fraud prevention. This finding is in line with the findings of Hailemarian [8] who found internal audit effectiveness as a good determinant of organizational control.

Internal auditors training, qualification and independence were statistically not significant in the joint model as their p-values were greater than 0.05, although with positive t-values. The findings were in line with those of Salma et al. [9] who investigated the determinants of internal audit effectiveness in the Sudan public sector and report positive but insignificant influence of these variables on internal audit performance. The descriptive statistic also confirms the inferential result.

The result in respect of Internal Auditors’ experience were both descriptively and inferentially statistically significant and positive as the t-value was positive and p-value 0.003<0.005. The findings corroborate those of Julius and Patrick [10] in their Rwanda revenue Authority investigation of internal audit effectiveness. On the whole, the apriori expectation were confirmed by the results of the data analysis.

Financial impropriety and mismanagement particularly at the Nigerian public sector require a shift from the traditional auditing which has been financially oriented to a more value investigative and analytical approach geared to preventing the malady from recurring. Internal auditing which is designed to safeguard assets against defalcation or other similar irregularities is expected to be carried out by personnel with distinct attributes. The study was conducted to examine how these internal auditors’ attributes help in fraud prevention in government MDAs in Akwa Ibom State, Nigeria.

Based on the findings of the study, it is concluded that fraud and fraudulent practices can be prevented through improvement in the effectiveness, independence, training, experience and qualification of the internal auditors in MDAs of government.

Recommendations

Based on the findings, it is recommended that conducive environment be created for internal auditors to function including regular training and re-training programs to update them on contemporary developments in fraud prevention techniques. There should be review of internal auditing policies in MDAs in line with global best practices and organization for Economic Development and Co-operation framework on public financial management models.

Acknowledgment

The authors would like to thank the internal auditors in MDAs of government in Akwa Ibom State for their willingness to respond to the research instruments with objectivity.

Policy Implications of the Findings

The implication of the findings is that public assets will not be misappropriated and socio-economic development would be enhanced to scale-up societal living standard. It would serve as measures to prevention of fraudulent activities and minimize wastages and draining away of the common wealth of the people by effective, efficient, independent and thorough internal auditing.

Suggestions for Further Researches

A further study can be conducted by extending the scope geographically to other States in Nigeria and other developing economies.

Bekiaris, K. et al. “Economic Crisis Impact on Corporate Governance and Internal Audit.” 11th European Academic Conference in Internal Audit and Corporate Governance, ACG, Oslo, Norway, 2013.

Etim, E.O. et al. “Public Sector Reforms and Accountability: The Nigerian Perspective.” International Journal of Business and Common Market Studies, vol. 11, nos. 1-2, 2016, pp. 116-127.

Monday, D.A. Akwa Ibom State Government: Report of the Auditor-General on the Accounts of the State. 2017.

Ali, A.M. et al. “Internal Audit in the State and Local Governments of Malaysia.” Southern African Journal of Accountability and Auditing, vol. 7, 2017, pp. 32-41.

Rafay, K. and B. Slakeel. “Attributes of Internal Audit and Prevention, Detection and Assessment of Fraud in Pakistan.” The Lahore Journal of Business, vol. 9, no. 1, 2020, pp. 33-58.

Bierstaker, J.L. et al. “Accountant Perceptions Regarding Fraud Detection and Prevention Methods.” Managerial Auditing Journal, vol. 21, no. 5, 2006, pp. 520-535.

IIA. The Standards for the Professional Practice of Internal Auditing. Institute of Internal Auditors, IIA Research Foundation, 2009.

Brogalas, P. et al. “Factors Affecting the Internal Audit Effectiveness in Malaysia Organizations.” Managerial Auditing Journal, vol. 30, no. 1, 2015, pp. 34-35.

Chambers, A.D. and M. Odar. “Factors Affecting Effectiveness of Internal Auditing in Tunisian Organizations.” Journal of Auditing and Accounting, vol. 20, no. 3, 2015, pp. 296-307.

Tarekegan, T.E. “Determinant of Internal Auditors’ Effectiveness: Case of Ethiopian Public Sectors.” International Journal of Advances in Management and Economics, vol. 4, no. 5, 2015, pp. 73-83.

Hella, D. and K. Mohammed. “Factors Affecting the Internal Audit Effectiveness in Tunisian Organizations.” Research Journal of Finance and Accounting, vol. 7, no. 16, 2016, pp. 2-10.

George, T. et al. “Determinants of Internal Audit Effectiveness in Decentralized Local Government Administrative Systems.” International Journal of Business and Management, vol. 11, no. 2, 2016, pp. 184-195.

Fetu, A. “Determinants of Internal Audit Effectiveness in Roads Construction Sector: Case Study in Ethiopian Roads Authority.” Managerial Auditing Journal, vol. 6, no. 5, 2016, pp. 194-216.

George, D. et al. “The Effect of Internal Audit Effectiveness, Auditor Responsibility and Training in Fraud Detection.” Journal of Accounting and Management Information Systems, vol. 16, no. 4, 2017, pp. 434-453.

Ayitenew, T. and E. Lakech. “Determinants of Internal Audit Effectiveness: Evidence from Gurage Zone.” Journal of Finance and Accounting, vol. 9, no. 19, 2018, pp. 15-25.

Alqudah, A. et al. “Extrinsic Factors Influencing Internal Auditors’ Effectiveness in Jordanian Public Sector.” Review of European Studies, vol. 11, no. 2, 2019, pp. 67-79.

Alemzewed, A. “Determinants of Internal Audit Effectiveness in Ethiopia: The Case of Selected Budgetary Public Sectors.” Managerial Auditing Journal, vol. 15, no. 4, 2019, pp. 182-186.

Armstrong, E. and A. Yindana. “Determinants of Internal Audit Effectiveness in Selected Hospitals within the Kumasi Metropolis.” Managerial Auditing Journal, vol. 24, no. 9, 2019, pp. 445-456.

Ngugi, G.G. “Determinants of Internal Audit and Its Effectiveness in the Public Sector in Kenya: A Case of the National Treasury.” Journal of Accounting and Management Information System, vol. 18, no. 3, 2020, pp. 43-47.

Mvelo, C.S. et al. “Determinant of Internal Auditing Effectiveness in Public Higher Education Institutions.” Academy of Accounting and Financial Studies Journal, vol. 25, no. 2, 202, pp. 1-8.

Hailemarian, S. “Determinant of Internal Audit Effectiveness in the Public Sector: Case Study of Ethiopian Public Sector Offices.” Management Accounting Review, vol. 62, 2014, pp. 442-453.

Salma, F.K. et al. “Determinants of Internal Audit Effectiveness: Case of Sudan Public Sectors.” Accountability Journal, vol. 42, no. 2, 2018, pp. 44-52.

Julius, K. and M. Patrick. “Determinant of Internal Audit Effectiveness of Public Sector: A Case Study of Rwanda Revenue Authority.” International Journal of Science and Research, vol. 7, no. 2, 2016, pp. 617-620.