+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

This paper seeks to examine how internal audit contributes to good governance in economic institutions especially in adverse conditions of Algeria. Due to the complexity involved in the design and implementation of, financial and operation systems, internal audit has become a strategic process that can go beyond the simple identification of financial irregularities and misstatements. The findings demonstrate how internal audit supports the application of governance principles and how it enhances the management of risks, the level of transparency and organisational performance. Cross-sectional research was done of which involved internal auditors and senior management on a sample of Algerian economic institutions. The study established positive and significant correlation between the quality of internal audit and governance. In addition, the research discovered that institutions with good internal audit mechanism in place benefit from better transparency, enhanced risk management and organizational performance. According to these findings, institutions should improve internal audit mechanisms with a view to being sustainable and gain competitive advantage.

Internal auditing is one among the four major pillars on which organizations depend to improve their governance. It is not only the control function which implies checking the compliance with the laws and regulations only, but it also embraces providing suggestions for increasing the performance of the institution and making strategic decisions. Through the rising complexities, regulations and competition in the world today, the role of internal auditing is rising in modern economic institutions. Internal auditing can be explained based on the following factors namely independence, professionalism and compliance with the international Auditing Standards[1].

1.2 Definition of Internal Audit

The most accepted definition of internal auditing is that internal auditing is an independent, objective assurance and consulting activity that helps an organization accomplish its objectives by bringing about improved efficiency. Internal audit enables an organization to meet its goals by taking a systematic way to assess and boost the success of risk management, internal control, and corporate governance. As stated by the Institute of Internal Auditors International internal auditing plays crucial role in increasing organizational efficiencies, increasing organizational transparency and assisting in decision making process[2].

1.3 The importance of internal audit

Therefore, internal audit has being viewed as crucial from the perspective of as having enhancing governance and establishing control over several activities within the institution. It aids the management in understanding potential risks and enable him or her to determine measures to take in order to address them. It also is responsible for relating the management of the institution to other parties such as investors and shareholders hence enhancing their confidence in the institution.

The most prominent benefits of internal audit are:

1. Detecting errors and fraud: Internal audit in a way assists in the identification of financial and administrative irregularities that could have an impact in the institutional image and financial performance.

2. Enhancing internal control: Internal audit enables enhancement of internal controls and check to ensure that the right policies and procedures are being followed.

3. Improving operational efficiency: by offering advice on how to make the organization more efficient and free up costs.

1.4 Types of internal audit

Internal audit varies to include several aspects according to the goals it seeks to achieve, including:

• Financial audit: Mainly deals with ascertaining the genuineness of the financial books of accounts of an institution to reflect the financial and economic events. The purpose of this kind of audit is to ascertain the conformity of the financial statements with GAAPs.

• Operational Audit: It is concerned with appraising the results of organizational activities in terms of the optimum use of resources. It is a kind of audit that seeks to assess the conformity of the operating processes to the achievement of their objectives and how this can be done.

• Conformity Audit: It makes sure that the organization follows internal and external legal requirements. It is one of the types that help the organization to meet legal and regulatory requirements of the company[3].

2.1 The Concept of Governance

Corporate governance policy in the economic institutions can be described as a system that is meant to control the link between the company’s leadership and its shareholders. Such principles include ways and means of Democracy, probity and integrity, freedom of information among others in the context of the institution. Actually, governance is not only a framework that guides the organization’s management but also a general system that defines the approach to strategic management decisions and distribution of assignments among subjects.

Governance is founded on certain rules that include: Proactive disclosure or communication of information, compliance with decision implementation, and equitableness to all parties. Appropriate use of the concept of governance improves the image of the institution and improves its ability to attract investment and expand the sphere of its activity.[4]

2.2 The Importance of Governance

For this reasons, governance is very crucial in enhancing the efficiency of management of economic institutions. It offers a guide that minimizes financial and administrative risks and on the same note increases the performance of organizations in the future. By applying the principles of governance, economic institutions can achieve several benefits, the most prominent of which are:

1. Enhancing transparency and accountability: Using governance reduces the risk of conflict of interests when offering information to investors and shareholders hence increasing their confidence in the management of the institution.

2. Increasing investments: A good corporate governance system brings about more investment attractiveness since it minimizes risks in the investment decisions and enhances the customer confidence in the sustainable nature of the organizations.

3. Improving financial and administrative performance: In its turn, governance is aimed at increasing efficiency of the institution’s operation and its management through enhancement of decision-making and distribution of tasks.

4. Reducing corruption: Therefore, with enhancement of the internal control systems plus clarity of the accountabilities of the governance systems; there are limited chances for financial and administrative corruption within institutions.[5]

2.3 Governance mechanisms

For institutions to adopt a set of mechanisms that can help in the achievement of governance objectives, there is need to put in place the following. Among these mechanisms are:

• Audit committees: They function as an extra body of the institution to scrutinize financial statements and compliance to accounting regulations. This committee also oversees the internal and external auditing for the organization.

• Boards of Directors: The Board of Directors major duty is to manage the organization’s policies and make major decisions. The Board of Directors is under pressure to ensure that it is making a positive contribution to the achievement of the strategic goals of the organization.

• Internal control systems: These systems help to improve the functioning of internal audit and reveal risks that can adversely influence the work.

This research was carried out on a selected group of economic institutions in Algeria with the general objective of assessing the contribution of internal auditing in enhancing governance. The data were collected by questionnaires because they were targeting samples such as the internal audit workers and members of the audit committees as well as the executive managers.

Descriptive research was adopted to analyze the extracted data and the (SPSS) program was employed to analyze the data and interpret the correlations between the variables.[6]

Section Two: Presentation and analysis of the results of the descriptive study.

In this section, we try to present and analyze the results of the descriptive study as follows:

- Validity and reliability of the studied sample

- Analysis of the characteristics of the studied sample

Analysis of the results of the descriptive study for the dimensions and axes of the study.

First requirement: Validity and reliability of the measurement tool

The validity of the questionnaire means that it represents the studied community well, that is, the answers we get from the questionnaire questions give us the information for which the questions were designed, while the reliability of the questionnaire means that if we redistribute the same questionnaire to another sample from the same community, the results will be close to the results of the first sample, and the validity and reliability of the questionnaire are tested with several tools, the most famous of which is the Alpha-Cronbach coefficient, as this coefficient takes values between zero and one, and most studies indicate that the Alpha-Cronbach coefficient must be greater than 0.60 in order for the measurement tool to be accepted, and for our study, the result of the stability test of the measurement tool is shown in the following table

Table (3-1): Represents the stability test of the measuring tool

| Statement | Number of phrases | Cronbach's alpha coefficient |

| Total value of all study variables | 28 | 0.904 |

Source prepared by the students based on the outputs of SPSS and Excel

It is clear from the table that the total value of the Cronbach's alpha reliability coefficient for all study variables was estimated at 0.904, which is greater than 0.6, indicating that the questionnaire measurement tool has a high degree of reliability and is amenable to study and analysis.

Second requirement: Analysis of the characteristics of the studied sample

The first section of the questionnaire included questions about the personal data of the sample members, which are: age, gender, educational qualification, professional experience. Below we review the distribution of sample members according to each variable with descriptive analysis. Section One: The distribution of sample members according to the gender variable is shown in the following table

Table (3-2) Distribution of sample members by gender

| Repetition | % | ||

| Gender | Males | 49 | 79 |

| Females | 13 | 21 | |

| Totall | 62 | 100 | |

Source: Prepared by the students based on the outputs of SPSS and Excel

Figure (3-1) summarizes the results of the previous table

Figure (3-1) represents the distribution of sample members according to gender

Source: Prepared by the students based on SPSS and Excel outputs.

From the previous table and figure, it is clear to us the distribution of percentages according to the gender of the sample individuals, where the large percentage was for males at 79%, while the females were at 21%, considering that this type of specialization is dominated by males, especially in the scientific field.[7]

Second Section: Age: Table (3-3) shows the age of the study sample individuals as shown below

Table (3-3): Distribution of sample members by age

| Repetition | % | |||||||

Age | <30 | 27 | 43.5 | |||||

| 31-40 | 14 | 22.6 | ||||||

| 41-50 | 15 | 24.2 | ||||||

| >50 | 6 | 9.7 | ||||||

| Total | 62 | 100 | ||||||

Source: Prepared by the students based on the outputs of SPSS and Excel

Figure (3-2) summarizes the results of the previous table

Figure(3-2): Distribution of sample members by age

Source: Prepared by the students based on the outputs of SPSS and Excel

From the previous table and figure, it is clear to us the distribution of percentages according to the age of the sample members, where the largest percentage was for the youth category (less than 30 years) at 43.5%, followed by the category from (41) to 50 years at 24.2%, then the category from 31 to 40 years at 22.6%, and finally the category from more than 50 years) at 9.7%, and this is an average indicator for the study sample in terms of years of experience in the practical field.[8]

Third Section: Educational Qualification

Table (3-4) shows the educational qualification of the study sample members.

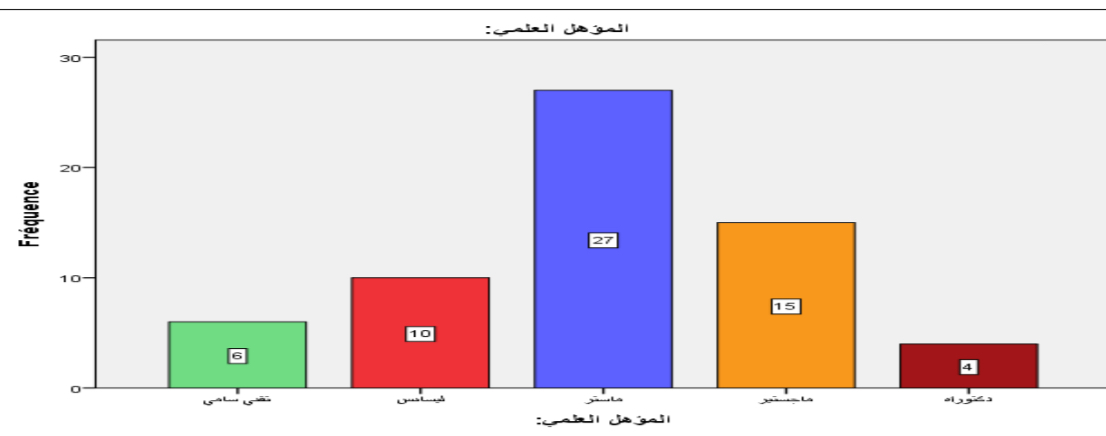

Table (3-4) Distribution of sample members according to educational qualification

| Repetition | % | ||

Educational qualification | Senior Technician | 6 | 9.7 |

| Bachelor's degree | 10 | 16.1 | |

| Master | 27 | 43.5 | |

| Master's | 15 | 24.2 | |

| PhD | 4 | 6.5 | |

| Total | 62 | 100 | |

Source: Prepared by the students based on the outputs of SPSS and Excel

Figure (3-3) summarizes the results of the previous table

Figure(3-3): Distribution of sample members according to educational qualification

Source: Prepared by the students based on the outputs of SPSS and Excel

From the previous table and figure, we can see the distribution of percentages according to the academic qualification of the sample members, where the largest percentage was for those holding a Master’s degree at 43.5%, followed by those holding a Master’s degree at 14.5%, then those holding a Bachelor’s degree at 16.1%, followed by those holding a Senior Technician’s degree at 9.7%, and finally those holding a PhD at 6.5%, which is a somewhat positive indicator for the sample members.

Fourth section: Scientific Specialization:[9]

Table (3-5) shows the scientific specialization of the study sample members.

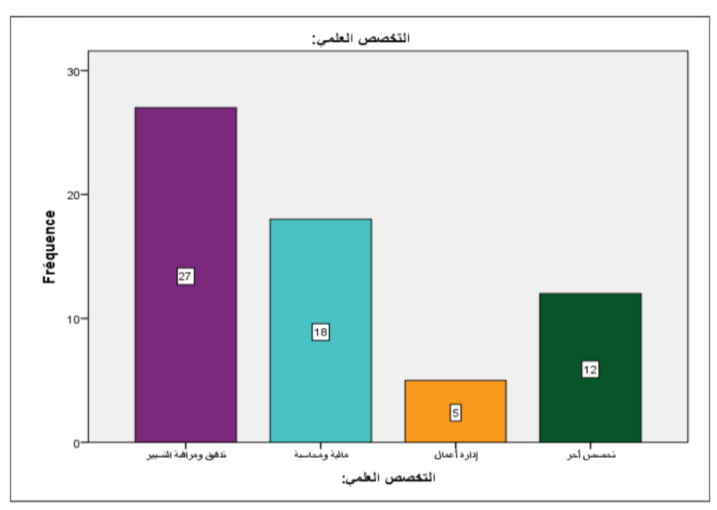

Table (3-5): Represents the scientific specialization of the sample members

| Repetition | % | ||

scientific specialization | Audit and control of management | 27 | 43.5 |

| Finance and Accounting | 18 | 29 | |

| Business administration | 5 | 8.1 | |

| Other | 12 | 19.4 | |

| Total | 62 | 100 | |

Source: Prepared by the students based on the outputs of SPSS and Excel

Figure (3-4) summarizes the results of the previous table.

Figure (3-4): represents the scientific specialization of the study sample members.

Source: Prepared by the students based on the outputs of SPSS and Excel

From the previous table and figure, it becomes clear to us the distribution of percentages according to the scientific specialization of the sample members, where the largest percentage is for those with a specialization in auditing and management control, at 43.5%, while those with a specialization in finance and accounting were at 29%, while other specializations not mentioned in the choices were at 19.4%, and the last comes the specialization in business administration at 8.1%.

Section Five: Job Title

Table (3-6) shows the job title of the study sample members.

Table (3-6) Distribution of sample members according to job title

| Repetition | % | |

Job title | Internal Auditor | 19 | 30.6 |

| accountant | 11 | 17.7 | |

| Financial Controller | 8 | 12.9 | |

| Comptroller | 11 | 17.7 | |

| Other | 13 | 21 | |

| Totall | 62 | 100 | |

Source: Prepared by the students based on the outputs of SPSS and Excel

Figure (3-5) summarizes the results of the table above.

Figure (3-5): Distribution of sample members according to job title

Source: Prepared by the students based on the outputs of SPSS and Excel

From the previous table and figure, we can see the distribution of percentages according to the job title of the sample members, where the largest percentage was for internal auditors at 30.6%, followed by those who hold different positions, financial manager, professors, professionals at 21%, followed by those who hold the position of accountant and bookkeeper at the same percentage of 17.7%, while the position of financial controller was at 12.9%, and this is an indicator of the average of the sample members.[10]

The third requirement: Descriptive statistical analysis of the information related to the questionnaire phrases. In this requirement, the information related to each phrase of the questionnaire is analyzed through descriptive statistical analysis of the questionnaire phrases.

- Results of the applied study: After studying and analyzing the applied aspect, we reached a set of results, which are:

-There is a relationship between internal auditing and corporate governance principles.

-There is a relationship between internal auditing and the principle of board of directors' responsibilities;

-There are no differences in the impact of internal auditing on corporate governance attributed to personal and functional variables. -The internal audit process contributes indirectly to ensuring shareholders' rights because it directly helps the board of directors, which is considered a representative of shareholders, to fulfill their obligations. -Since the internal audit function is part of the company's organizational structure, it is a function closely related to senior management and is subject to its orders.

-The internal audit mechanism is considered one of the important functions in the company because it provides support to the board of directors, the audit committee, and the external auditor by evaluating the internal control system and reviewing it to manage risks, but it cannot achieve the principles of governance alone, but other mechanisms greatly help in implementing governance.

The need to reorganize the internal audit function in companies to ensure its independence, objectivity, and the efficiency of its operations.-Obligating companies to work according to the basic rules of corporate governance, which are summarized in transparency, accountability, fairness, and disclosure of the extent of their work in annual reports, with the imposition of penalties on anyone who violates the proper application of these rules.- The necessity of exploiting technology and modern means to keep pace with the development of companies and their activities in the internal audit process so that governance reaches the required level of performance effectiveness.- Maintaining a sufficient and fair level of disclosure and transparency of important information in financial reports and making it available to all stakeholders to benefit from it at the appropriate time.- Holding seminars, conferences, forums and training programs by those interested in corporate governance rules for the relevant parties to be aware of the past and present and prepare for the future.- The necessity of holding training courses for internal auditors with the aim of providing them with sufficient knowledge of the internal audit standards issued by the Institute of Internal Auditors and then working to adopt them gradually in companies.

The authors declare that they have no conflict of interest

No funding sources

The study was approved by the Alkut University College

Thanaa Al-Qabbani and Nader Shaaban Al-Sawah, Internal Auditing in Light of Electronic Operation, Dar Al-Jamiah, P29 Alexandria, 2006.

Khaled Ragheb Al-Khatib, Insurance from the Accounting and Auditing Perspective, Dar Al-Kaun, Amman, 2000, p. 162

Khalaf Abdullah Al-Wardat, Internal Auditing between Theory and Practice, First Edition, Al-Warraq Foundation for Publishing and Distribution, Jordan, 2006, p. 33-34.

Zahra Tawfiq Sawad, Auditing and Auditing, First Edition, Dar Al-Rayah for Publishing and Distribution, Amman, Jordan2009, p. 89 p.

Adnan bin Haider bin Darwish, The Role of Corporate Governance and the Role of the Board of Directors, Union of Arab Banks, 2007, 20

Youssef Mahmoud Jarbou, Auditing, First Edition, Al-Warraq Foundation, Amman, 2000, p. 128

Hassiani Abdel Hamid, The Importance of Transitioning to International Accounting Standards and Financial Information as a Framework for Activating Corporate Governance, Unpublished Master's Thesis, University of Algeria 3, 2009-2010, p. 152

Rola Abdel Majeed Inshasi, The Role of Corporate Governance in Improving the Internal Audit Function, Unpublished Master's Thesis, Islamic University of Gaza, September 2015, p. 21

Omari Aisha, The Role of Internal Audit in Improving the Quality of Banking Services from the Point of View of Bank Employees, Graduation Thesis Imd Management Sciences, 2018/2017.

Youssef Saeed Youssef Al-Mudallal, The Role of the Internal Audit Function in Controlling Financial and Administrative Intelligence, Unpublished Master's Thesis, Islamic University of Gaza, Palestine, 2007, p. 76