+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2788-9491

ISSN (Online) : 2788-9505

The objective of the research is to examine the variations in the exchange rate and their influence on the trade balance in Iraq. This will be accomplished by employing a descriptive and quantitative methodology to evaluate the impact of the exchange rate on the trade balance. The empirical analysis is conducted for the period 2004–2022, with the aid of VAR model and impulse response function to estimate the degree of the exchange rate volatility on the trade balance of Iraq. The evidence points towards a direct path dependency between the exchange rate, measured by US dollars per dinar, and exports and an inverse and negative path dependency with imports.

The exchange rate is viewed as the key monetary instrument, if not the most critical one, for it indeed impacts several major economic variables in all countries. A currency strength and impact it has on the relationship between domestic and foreign prices are defined by it. Exchange rate is also an important factor under competition since it forms a link between the economy of a country and the rest of the global economy. This research aims at establishing the effects of exchange rate shocks on the trade balance of Iraq in the period 2004-2022. The purpose of this study is to analyze the effect of parallel exchange rates on the trade balance of Iraq and to analyze the fluctuation of these rates in the research period.

Problem Statement

The research question is to evaluate the effectiveness of Central Bank of Iraq’s action in preventing the increase in exchange rates with the view of achieving monetary stability. This is done by establishing the effect of the exchange rate of the Iraqi dinar on the trade balance for the period under study.

Research Hypothesis

We hypothesize that reducing the value of the currency (dinar) has a significant and positive impact on the trade balance surplus.

Significance of the Research

The importance of this research is evident from the effect of exchange rate as one of the macroeconomic factors that determines the trade balance. In the study, the focus is made on the role of the trade balance and its impact on the identification of the state of the economy. In addition, the study seeks to develop relevant and effective recommendations for the minimization of a deficit in the trade balance in Iraq.

Research Objectives

The study aims at analyzing the effect of the parallel exchange rate on the trade balance of Iraq. The purpose, therefore, is to assess the effect of parallel exchange rate on Iraq’s trade balance for the period 2004-2023. The research also aims at identifying how quickly the trade balance responds to changes in the exchange rate, an important parameter for policy making.

In this case, the study uses an analytical-descriptive research approach to operationalise and describe the research variables. In addition, it relies on a quantitative or measurement method in order to determine the impact of exchange rate for trade balance.

Previous Studies

There is research done by Bakhtiar [1] in a paper with the title “The Impact of Economic Variables on the Trade Balance Using the Co-integration Approach.” The study intended to establish the effect of economic factors and their interactions on the trade balance. The authors also discovered a highly significant association between national income and the trade balance, which implies that an increase of one unit in national income leads to an increase of 0.129 in the trade balance. The report recommended that action should be taken to raise the national revenue of Iraq because this would positively impact on the trade balance. Moreover, it stressed the necessity of the economic diversification of Iraq

Khaleel and Jassim [2] conducted a study that aim to analyze the impact of exchange rate fluctuations of the Iraqi dinar on the trade balance in the period 1990-2016. The research problem focused on fluctuations of exchange rates over the period under consideration and its impact on the trade balance comprising of exports and imports. The study also made a connection between these variables. The suggestions extended the conclusions of the last study; the need to diversify Iraq’s export base from a rentier base that mainly depends on oil to a diversified base from many resources. The proposal of diversification was put up as a strategic measure to bolster Iraq's trade balance by amplifying trade surpluses through augmented exports and diminished imports

Research Structure

The research is divided into several axes. It includes the theoretical framework that encompasses the concept of exchange rates, their types and the definition of the trade balance and its various forms. The research focuses on the analytical aspect of the impact of exchange rate fluctuations on the trade balance during the research period (2004-2022). Finally, the research concludes with findings and recommendations.

Firstly: The Theoretical Impact of Exchange Rates

The exchange rate is considered one of the most crucial tools of effective monetary policy to safeguard the Iraqi economy from external shocks it may encounter.

Definition of Exchange Rate

The term refers to the exchange rate between foreign currency and local currency. Exchange rate refers to the price at which one unit of foreign currency may be obtained in terms of the local currency or the quantity of local currency required to exchange for one unit of another foreign currency. In this sense, exchange refers to the act of substituting one form of currency for an equal value of another form of currency, for as converting dollars into dinars or euros into dollars [3].

Types of Exchange Rates

Nominal Exchange Rate: It refers to the process of determining the worth of a currency in a particular nation, which may then be traded for the value of another country's currency. The exchange is conducted according to their respective rates. The nominal exchange rate is established based on the demand and supply of the domestic currency in the foreign exchange market at a certain point in time [4].

Further Subtypes of Nominal Exchange Rate Include

Official Government Exchange Rate: This rate is concerned with official current exchanges.

Parallel Exchange Rate

The term "rate" refers to the utilization of multiple nominal exchange rates for the same currency within a country's non-official markets, all occurring simultaneously.

Real Exchange Rate

It denotes the exchange rate at which one unit of the local currency can be exchanged for a certain amount of foreign products and services. The indicator serves as a measure of the competitiveness of local exports and economic organizations utilize it to inform their decision-making processes. For instance, when export revenues and production costs of exported goods both increase by the same percentage, it does not automatically lead to an increase in exports. This is because the increase in revenues may not correspond to a proportional increase in the profits earned by exporters [5].

Effective Exchange Rate

The effective exchange rate measures the actual purchasing power of a currency relative to foreign currencies. The index evaluates the fluctuation of the domestic currency's value relative to other currencies by indicating the rate of change in the currency exchange rate over a specific time period. The effective exchange rate encompasses both the nominal effective exchange rate and the real effective exchange rate.

Secondly: The Theoretical Framework for the Concept of Trade Balance

What is the Trade Balance?: The trade balance is a crucial aspect of the balance of payments, comprising all tangible aspects associated with the flow of commodities and services, including exports and imports, between a particular country and other countries during a given timeframe. The trade balance is a metric used to quantify the disparity in worth between a country's exports and imports of commodities and services. This metric is utilized to evaluate the comparative robustness of regional economies. A trade surplus occurs when the volume of exports surpasses that of imports. On the other hand, if the quantity of goods and services being sold to other countries is lower than the quantity being bought from them, it signifies a negative balance of trade. The trade balance is a vital indicator for assessing a nation's economic success and its level of involvement in the global market [3].

Trade Balance Formula

The trade balance is calculated as the difference between the total exports (X) and the total imports (M) for a country:

Trade Balance = Total Exports (X) - Total Imports (M)

Structure of the Trade Balance

The trade balance is divided into two accounts:

Visible Trade Account (Goods): This account comprises all items pertaining to the commerce of physical products, comprising both outbound shipments and inbound acquisitions. The visible trade balance refers to the disparity between exports and imports in this account. A deficit occurs when imports surpass exports, while a surplus occurs when exports surpass imports [3]

Invisible Trade Account (Services): This account encompasses all services traded between the country and other nations, including transportation services, insurance, tourism, governmental services, foreign investment revenue and advisory services. Consultancy services refer to services rendered by foreign capital to the country or services offered by domestic capital to foreign enterprises

Thirdly: The Relationship Between Exchange Rates and Trade Balance

A correlation exists between a country's trade balance and the domestic exchange rate of its currency. Fluctuations in the currency rate can either enhance or diminish the trade balance. When the value of the local currency rises compared to foreign currencies, it might worsen the balance of payments and disrupt the trade balance. A rise in the exchange rate can lead to a surge in imports from foreign countries and a decline in exports, as the elevated costs of domestic goods in the foreign currency market make them less competitive. In contrast, depreciating the local currency's exchange rate can result in a surge in exports and a decline in imports, as the prices of domestic goods become more competitive in international markets. Nevertheless, alterations in exports or imports due to fluctuations in the exchange rate do not transpire readily or swiftly; rather, they are contingent upon the adaptability of the goods and services being traded. If the imported items are deemed indispensable, a reduction in the exchange rate may not exert any influence on the importation of those commodities, given their essential nature. According to Appleyard et al. [4], there is a direct relationship between the elasticity of demand and the influence of the exchange rate on the trade balance. The greater the elasticity of demand, the more significant the impact of the exchange rate.

Fourth: Formulation of the Estimation Model and Methodology

Our research focuses on the quantitative component, which is ideal for analyzing the correlation between exchange rate volatility and the trade deficit in Iraq. We utilize the Vector Autoregression (VAR) model and the Impulse Response Function to quantify the response of the dependent variable to changes in the independent variables. Employing different initial and follow-up tests involving: testing the stability of time series, calculating the lag length of the vector autoregressive model, analysis of response functions and the variance decomposition analysis.

Indicators Used in the Estimation

The research involved three variables; two dependent variables and one independent variable. Symbols were utilized based on codes available in the International Monetary Fund (IMF), as outlined in the Table 1.

Table 1: The International Monetary Fund (IMF)

Semantics | Symbol | Description |

Exports | EXP | Dependent Variable |

Imports | IMP | Dependent Variable |

Parallel Exchange Rate | EXCH | Independent Variable |

Time Series Stationarity Test

The unit root test is an important part of the analysis of time series for economic variables because it allows to establish the stability of the data. This is done in order to avoid so-called misleading regression and to obtain accurate economic conclusions. Based on the results of the Augmented Dickey-Fuller (ADF) and Phillips-Perron tests, it was identified that the used time series data for economic variables were non-stationary at this level. Consequently, a unit root test was performed using first differences, revealing that the variables in issue were stable at the first difference level with a significant level of 5%. The source cited is Kerry Patterson's book from 2011, page 189 (Table 2).

Table 2: Illustrates Unit Root Tests for the Variables

The variable | The type of test | The level | Test value | p-value | The result |

EXCH | ADF | Level | -1.44575 | 0.537 | Unstable |

First D | -3.081002 | 0.025 | Stable | ||

Phillips-perron | Level | -1.406656 | 0.5571 | Unstable | |

First D | -3.857386 | 0.0237 | Stable | ||

EXP | ADF | Level | -2.226399 | 0.2048 | Unstable |

First D | -4.147957 | 0.0065 | Stable | ||

Phillips-perron | Level | -2.528288 | 0.1266 | Unstable | |

First D | -5.031772 | 0.0009 | Stable | ||

IMP | ADF | Level | -2.072341 | 0.2567 | unstable |

First D | -3.625695 | 0.0176 | Stable | ||

Phillips-perron | Level | -1.550529 | 0.4861 | unstable | |

First D | -2.555008 | 0.121 | Unstable |

The table was prepared by the researcher using the "Eviews 10" software

The first branch: Johansen-Juselius Cointegration Test

A prerequisite for conducting this test is that the time series for these variables must be of the same magnitude and have the same level of integration. Once the order of integration for each variable has been determined by conducting a unit root test on the variables involved in the research, this test serves as the second step in the testing procedure. After integrating these time series with a first-order process, the subsequent task is to verify the presence of a long-term equilibrium relationship between the variables through the application of the Johansen-Juselius Cointegration Test.

The Johansen-Juselius test stands out from other tests because it is particularly appropriate for analyzing situations involving numerous variables. When dealing with many variables that exhibit diverse patterns in the common integration vector, Johannsen and Juselius provide two statistical tests: The Trace Test and the Maximum Eigenvalue Test.

Firstly: Trace Test

Where this test takes the following mathematical form:

λTrace(r/n)=−Ti=r+1∑nrln(1−λ~i)r=0,1,2,…,n−1

Where:

T : The sample size

r : The number of cointegrating vectors

n : The number of variables in the model

Johannsen and Juselius developed a table of critical values for the trace statistic in 1990. After calculating the computed value of , it is compared with the tabulated critical value. The following cases are considered based on the rank of the cointegration:

If the computed is greater than the tabulated critical value, we reject the null hypothesis (H_0) and proceed to the next test

If the computed is less than the tabulated critical value, we accept the null hypothesis (H_0) and stop the test at this point

This process is repeated for each test until the completion of the entire set of tests (Table 3).

Table 3: Illustrates the Impact Test for the Variables: Exchange Rate, Exports and Imports

Trace Statistic test | |||

Hypothesized | Trace Statistic | Critical Value | Prob |

None | 49.18655 | 29.79707 | 0.0001 |

At most 1 | 17.14063 | 15.49471 | 0.028 |

At most 2 | 1.46841 | 3.841466 | 0.2256 |

The table was prepared by the researcher using the "Eviews 10" software

Secondly: Maximum Eigenvalue Test

The mathematical formula for this test is represented as follows:

λTrace(r/(n+1))=−T⋅rln(1−λ~i)r=0,1,2,…,n−1

where, (λ) is the Maximum Eigenvalue, (T) is the sample size, (r) is the number of cointegration vectors and (n) is the number of variables in the model.

This formula is a test for the null hypothesis that the sum of cointegration vectors is equal to r, compared to the alternative hypothesis that the sum of cointegration vectors is equal to r+1. The investigation revealed that the variables in the basic model became stationary after undergoing first differences, indicating an integration of order one (1) I. Hence, the subsequent stage involves identifying enduring cointegrating associations, which necessitates first ascertaining the optimal lag duration (Table 4).

Table 4: Illustrates the Maximum Eigenvalue Test for the Impact of the Variables Exchange Rate, Exports and Imports

Max-Eigen Statistic test | |||

Hypothesized | Max-Eigen Statistic | Critical Value | Prob |

None | 32.04592 | 21.13162 | 0.0010 |

At most 1 | 15.67222 | 14.26460 | 0.0298 |

At most 2 | 1.468410 | 3.841466 | 0.2256 |

The table was prepared by the researcher using the "Eviews 10" software

Determination of Optimal Lag Lengths

The lag length was determined based on five distinct criteria: The Schwartz Criterion (SC), the Hannan-Quinn Criterion (HQ), the Akaike Criterion (AIC), the Final Prediction Error (FPE) Criterion and the likelihood ratio (LR) test. According to the test findings, the best lag length was determined to be 1 (Table 5).

Table 5: Determination of Optimal Lag Lengths

VAR Lag Order Selection Criteria | ||||||

Endogenous variables: EXCH EXP IMP | ||||||

Exogenous variables: C | ||||||

Date: 11/03/23 Time: 21:32 | ||||||

Sample: 2004 2022 | ||||||

Included observations: 17 | ||||||

Lag | LogL | LR | FPE | AIC | SC | HQ |

0 | -507.4099 | NA | 8.56e+20 | 56.71221 | 56.86061 | 56.73267 |

1 | -468.7215 | 60.18196* | 3.23e+19* | 53.41350* | 54.00708* | 53.49535* |

2 | -461.3297 | 9.034389 | 4.30e+19 | 53.59219 | 54.63096 | 53.73542 |

* indicates lag order selected by the criterion | ||||||

LR: sequential modified LR test statistic (each test at 5% level) | ||||||

FPE: Final prediction error | ||||||

AIC: Akaike information criterion | ||||||

SC: Schwarz information criterion | ||||||

HQ: Hannan-Quinn information criterion | ||||||

Firstly: VAR Model Estimation

When conducting a model estimation utilizing the Vector Autoregression (VAR) approach, we utilize the first differences of variables as the estimation method. Additionally, we consider the best lag length of 1 for the lag order, as suggested by Gujarati et al. [6]. It is important to note that we analyze each equation individually.

Model 1: Response Function of Exports and Imports to the Exchange Rate

EXP = 0.753066494017*EXP (-1)-26.4637312815*

EXCH(-1)-13755.328242

MP = 0.700468291804*IMP(-1) +16.1900157257*

EXCH(-1)+35182.1016665

Explanation of the Results

Regarding the response of the exchange rate to exports and imports, we observe that a decrease in the Iraqi dinar against the US dollar (exchange rate) has a positive effect on exports. The relationship is inverse, as indicated in the equation above. This means that as the value of the dinar decreases, Iraqi exports increase, leading to an improvement in the Iraqi trade balance.

Conversely, the impact is opposite for imports. As the value of the Iraqi dinar increases against the US dollar, it leads to an increase in imports, contributing to a trade deficit in the Iraqi trade balance.

Secondly: Impulse Response Functions (IRFs)

In our previous studies of VAR models, we have explained Impulse Response Functions (IRFs). This study entailed the application of a series of structural shocks to the model, followed by the observation of the outcomes and the analysis of the graphical representations (IRFs).

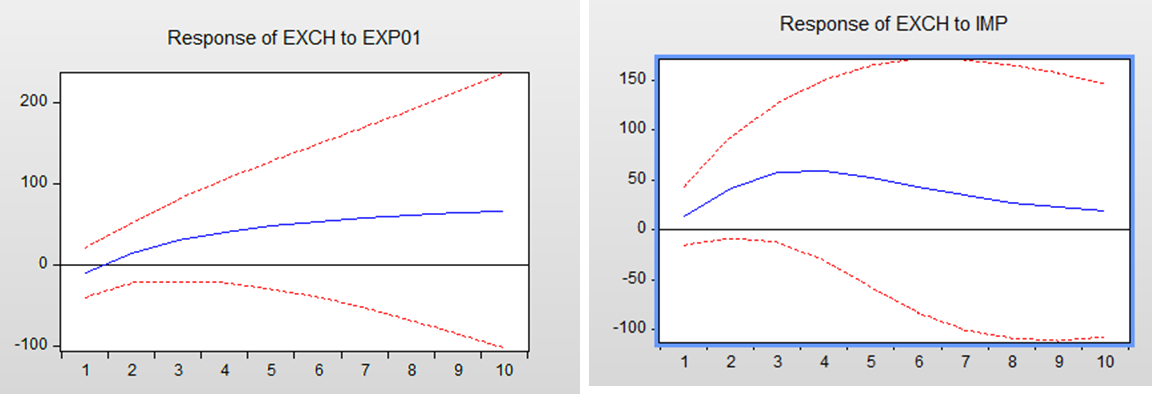

Impulse Response Analysis pertains to the impact of a sudden change in one variable on itself and other variables within a certain timeframe. Impulse response functions (IRFs) represent the total effect of the internal variables to a shock in a single variable in the model. The amount of shock is calculated in terms of standard deviations and the information is presented visually. The variables in the original model exhibit a prompt response to different shocks delivered to other variables (Figure 1).

Figure 1: Illustrates the Impulse Response Functions

For our analysis of the impulse response functions, we will introduce a sudden change to the variables related to trade policy and observe the subsequent impact on the exchange rate. The test findings are depicted in Figure 1, with the blue line representing the response to the shock and its temporal variation during the research period. The confidence interval is represented by the red line.

Interpretation of the Results

When examining the effect of a trade balance deficit on variables, we find that a slight random disturbance would lead to an increase in exports. This effect is most noticeable in the second and third periods, specifically during the shock in late 2013, as seen in the equation above. To be more explicit, a rise in the exchange rate between the dollar and the dinar will have a positive impact on the trade balance and conversely, this effect will be more significant over a longer period of time. This is consistent with economic theory and the impulse response function depicted above.

Likewise, when the currency rate (dollar against dinar) increases, imports will be negatively impacted. As the value of the dollar rises in relation to the dinar, the amount of imports will decline, resulting in a higher imbalance in Iraq's trade balance.

Third: Variance Decomposition Analysis

This is a process through which we can identify the proportion of variance caused by one variable in itself and in other variables [7]. In our study, we will examine the relationship between the variables of the trade balance and the exchange rate included in our model.

According to the data presented in Table 6, the variance analysis results reveal that the whole fluctuation in the trade balance (exports and imports) during the first year can be traced to a single variable. Subsequently, there is a decline, with exports dropping to 92% and imports to 87% by the fifth year. The export rate remains constant at 92% in the ninth year but the import rate is at 86%. Given this decrease, it is evident that changes in exchange rates have a more significant influence on imports rather than exports.

Table 6: Illustrates the Variance Decomposition Analysis for the Variables Under Investigation

Period | S.E. | EXP01 | EXCH |

1 | 21813.01 | 100.0000 | 0.000000 |

2 | 29110.14 | 97.94120 | 2.058805 |

3 | 30553.79 | 94.85142 | 5.148585 |

4 | 30811.42 | 93.27247 | 6.727535 |

5 | 30908.06 | 92.97319 | 7.026806 |

6 | 30914.29 | 92.94999 | 7.050013 |

7 | 30925.03 | 92.95282 | 7.047178 |

8 | 30940.73 | 92.95570 | 7.044303 |

9 | 30946.59 | 92.95102 | 7.048978 |

10 | 30947.60 | 92.94663 | 7.053368 |

Period | S.E. | IMP | EXCH |

1 | 8498.666 | 100.0000 | 0.000000 |

2 | 12156.11 | 95.38483 | 4.615174 |

3 | 13675.65 | 90.27060 | 9.729402 |

4 | 14145.60 | 87.75796 | 12.24204 |

5 | 14240.43 | 87.22524 | 12.77476 |

6 | 14255.40 | 87.24042 | 12.75958 |

7 | 14274.47 | 87.19767 | 12.80233 |

8 | 14304.77 | 87.09257 | 12.90743 |

9 | 14338.18 | 87.00443 | 12.99557 |

10 | 14368.71 | 86.95135 | 13.04865 |

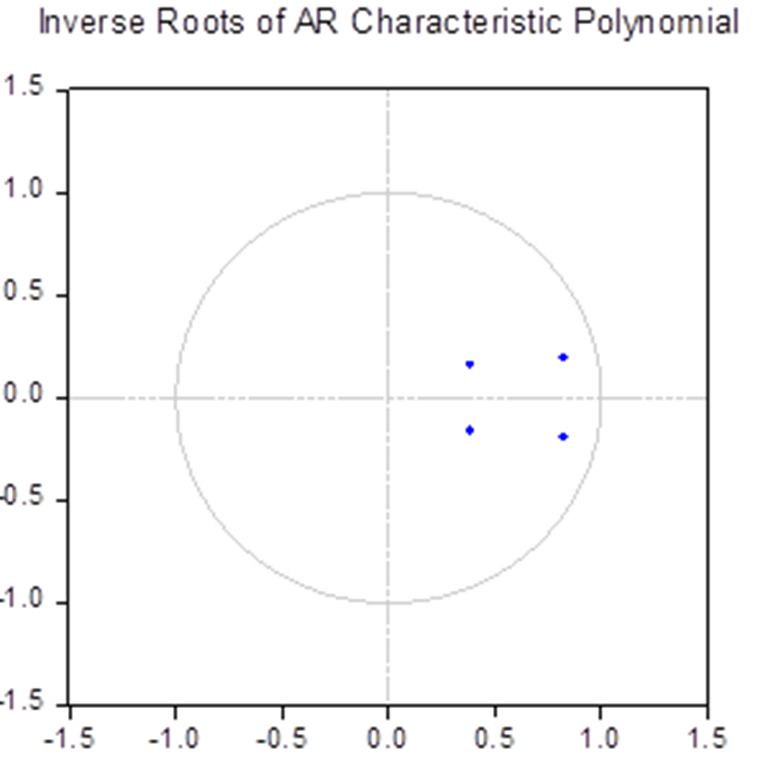

Results of the VAR Model Stationarity Test

As depicted in the Figure 2, all the variables utilized in the study are contained within the unit circle. Given that the VAR model is applied to roots with magnitudes exceeding one, it is apparent that the vector autoregression is stable. This enables us to assess the impact of the model's swings in exchange rates on Iraq's balance of trade, including exports and imports.

Figure 2: Inverted Roots of the Model

The Researchers Arrived at Several Results, With the Most Prominent Being

The fluctuations in the exchange rates of the Iraqi dinar against the US dollar in the parallel market have a clear impact on the trade balance in Iraq during the research period, especially on exports, as evident in our study

There is an inverse relationship between the exchange rate of the parallel dinar and exports during the research period. Whenever the dinar depreciates against the dollar, the competitiveness of Iraqi exports increases, leading to higher exports abroad

There is a causative relationship between the exchange rate and imports. As the dinar appreciates against the dollar, the purchasing power of citizens increases, resulting in higher demand for imports and consequently causing a trade deficit

Based on the Derived Results, We Attempted to Provide Some Suggestions and Recommendations

Work on maintaining or stabilizing the exchange rate of the Iraqi dinar against foreign currencies by adopting a set of monetary policies based on economic indicators that have an effective impact on the exchange rate

Increase the flexibility of the production sector by stimulating and supporting various productive sectors and projects, diversifying agricultural and industrial exports to enhance competitiveness abroad and avoiding reliance solely on oil exports

Develop a supportive fiscal and monetary policy for economic growth, targeting increased exports, reduced imports and promoting local production to decrease the trade deficit. Diversify policies and also reduce the drain of foreign currency by finding local solutions and alternatives

Bakhtiari, A.T. and O. Abbas. “The Impact of Economic Variables on the Joint Trade Balance.” Kirkuk University Journal of Administrative and Economic Sciences, vol. 11, no. 1, 2021.

Khaleel, I.A. and I.A. Jassim. “The Impact of Exchange Rate Fluctuations on the Trade Balance for the Period 1990-2016.” Baghdad College of Economics Journal, no. 58, 2019.

Carbaugh, R.J. International Economics. 17th ed., Cengage, 2021.

Appleyard, D. et al. International Economics. 5th Ed., McGraw-Hill, 2006.

Ameen, S. Exchange Rate Policy as a Tool for Balancing Imbalances in the Balance of Payments. 1st ed., Hassan Al-Asryah Printing and Publishing Library, 2013.

Gujarati, D.N. et al. Basic Econometrics. 2009.

Neusser, K. Time Series Econometrics. Springer International Publishing, 2016.